DeFi lending market update, Aave vs Compound risk appetite, it's GHO-time, EthCC risk & lending catch-up, Q&A with Term Finance,...

DeFi lending market update, Aave vs Compound risk appetite, it's GHO-time, EthCC risk & lending catch-up, Q&A with Term Finance,...

Issue #47 of The State of DeFi Lending newsletter

Welcome to issue #47 of The State of DeFi Lending, a newsletter covering the highlights of lending markets in DeFi.

In this issue we cover:

TokenTerminal released a timely update on the DeFi lending space: Year to date, the lending sector has seen an increase in active loans from $3.5bn to $5.5bn with Aave holding a 50% market share. This report is a must-read for anyone in the lending space.

BlockAnalitica asked the question whether “Aave is more conservative than Compound?” based on RiskDAO’s smart LTV formula. The answer to this question is affirmative and highlights how much lending protocols should adopt a proactive & dynamic risk management.

Aave’s stablecoin GHO was activated on Ethereum mainnet less than two weeks ago. Circulating GHO amounts to $7.8m but so far the stablecoin has struggled to defend the peg.

EthCC Paris took place last week. Lending risks & security got featured across a number of sessions. We caught up with the most relevant ones so you don’t miss out.

Dion from Term Finance sat down with us to explain how Term is differentiated from existing lending protocols and where opportunities for the protocol are.

Read below for more…

News

DeFi lending is a growing sector: YTD active loans grew from $3.5bn to $5.5bn (+57%) according to TokenTerminals “Weekly Fundamentals” series.

Aave remains the 800lbs gorilla with a market share of ~50% and active loans of $2.8bn (up $0.7bn YTD). As much as size matters, the fastest growing protocols are Radiant Capital and Morpho with active loan growth rates of 370% and 63%, respectively. Radiant Capital's growth has been significantly influenced by its expansion to the BNB Chain.

TokenTerminals attributes the rebound in borrowing demand to the improvement in market sentiment. Aggregated active loans peaked at $24.1b during the market cycle top in Q4’21 and bottomed out in Q1’23 at $3.5b, a drawdown of over 85%. Since then, active loans have been on a general uptrend, as the price of Bitcoin has simultaneously risen from ~$16k to ~$30k.

Risk management in Aave v3 and Compound v3 lending markets

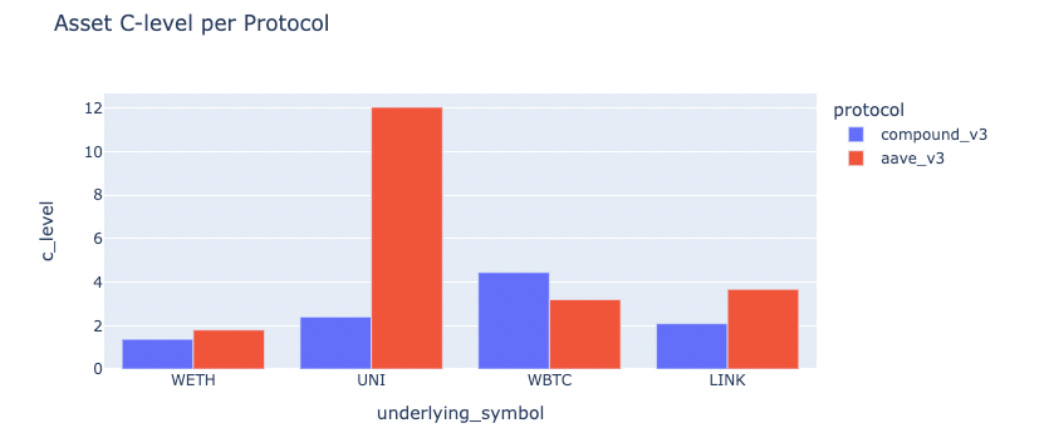

Risk management is of paramount importance to ensure the stability and sustainability of lending markets. In a recent collaboration between Block Analitica and RiskDAO, an innovative approach to determining liquidation thresholds and loan-to-value (LTV) ratios has been explored and applied to Aave v3 markets.

The heart of the risk management approach lies in a formula proposed by RiskDAO, which introduces a crucial parameter: the confidence level factor (c). This factor represents risk appetite and various assumptions, influencing insolvency probabilities. By tweaking the value of c, lending platforms can adjust their LTV ratios accordingly. The higher the c-level, the lower the risk appetite. The below graphic highlights different c-levels for select pairs across Aave v3 & Compound v3.

DEX liquidity emerged as a critical determinant in choosing the confidence level factor.

The research article sheds light on the conservative nature of Aave v3 liquidation thresholds and the importance of dynamic risk management in DeFi lending markets. By understanding the confidence level factor and its relationship with LTV ratios, lending platforms can better navigate market conditions and provide a safer environment for users. The research also highlights that risk management is a pro-active, dynamic process that requires constant adjustments based on market moves.

Aave’s long-awaited GHO finally launched on ETH Mainnet on 15 July. The Aave community has high hopes for the stablecoin as accrued interest goes directly to the Aave DAO treasury.

Circulating supply hit $2.5m within 2 days post-launch. At the time of writing, approx $7.8m GHO have been minted across 292 holders. ~50% of the circulating GHO supply sits in the Balancer pool.

GHO has struggled to hold its USD-peg thus far, averaging $0.982 and dropping as low as $0.9776.

To ensure stability of GHO, Aave Companies is proposing to introduce the GHO stability module, inspired by MakerDAO’s PSM that enables the seamless conversion of two tokens at a predetermined ratio.

EthCC and Paris Blockchain Week happened last week. For those who could not attend, we summarise some key talks & presentations that touch the DeFi lending space.

BProtocol/RiskDAO’s Yaron Velner presents an approach to risk management in DeFi lending markets that aims to increase transparency, predictability, and efficiency by using a Uniswap formula for LTV ratios and other risk parameters. Concepts of this talk have been reflected in BlockAnalitica/RiskDAO’s work around Aave’s risk appetite (see first article in today’s newsletter).

Paul from Morpho Protocol talks about a metamorphosis that DeFi lending needs. Paul suggests the sector will bifurcate into Decentralized Brokers (eg Aave/Compound = product-oriented and rely on statistics and economic models) & Protocols which are more primitive and independent and provide a foundation for future abstraction layers to be built on top. Morpho is developing a new protocol that aims to establish core primitives and remove the need for the DAO to be trusted.

Mikhail from Gearbox Protocol shed some light onto the protocol’s architecture and key elements. The protocol allows users to open a credit account, provide funds, and take a margin loan from the pool. The funds can then be managed by the user to build any strategy they want. However, users cannot withdraw money into their pocket; all funds in the credit account are used as collateral. The speaker discusses the Gearbox Risk Framework, which aims to provide full transparency for the community (check out the Gearbox risk dashboard created by RiskDAO). The strategy for scaling Gearbox involves starting with blue-chip protocols, limiting exposure to any protocol, and continuously increasing the limit for exposure to any particular token as it proves to be reliable.

For those readers who are inclined to go deeper down the rabbithole, here is a selection of additional videos:

Short news & announcements

ARC: Aave and Harmony Joint Recovery Plan Following the Harmony Blockchain Hack

Fuji Finance launches v2 as a cross-chain money markets aggregator

Geist Finance shutting down as funds from Multichain-hack cannot be recovered

Compound Labs introduces Encumber: Enabling Non-custodial DeFi

WuBlockchain report on RWAs, with a focus on MakerDAO’s execution strategy

Q&A with Dion Chu from Term Finance

Short description

Term Finance is a decentralized non-custodial lending protocol that allows users to lend or borrow on a fixed rate basis. This is facilitated through weekly auctions, where potential lenders and borrowers submit their respective asks and bids. The system then determines a market clearing interest rate, enabling lenders and borrowers who meet this rate to transact.

Term Finance's auction model is unique as it originates loans at scale without slippage, bid-offer spread, or other hidden transaction costs, which are common in other variable and fixed rate lending protocols. Term Labs raised $2.5m in a seed round in Feb 2023.

Prior to co-founding Term, Dion (@dionchu) advised various NFT and DeFi projects while running a small family office focused on systematic trading. He started his career in TradFi, spending time at D.E. Shaw, the Federal Reserve, Board of Governors, Jefferies and Capula Investment Management. He holds a B.A. from Cornell in economics and a J.D. from Harvard Law School.

Term Finance’s auction-based, fixed-rate model is a relatively unique product that’s different from the large peer-to-pool protocols. What problem is Term solving and in how far will you compete with Aave or Compound?

In many ways, we are complementary to Aave/Compound. Like those protocols, Term focuses on overcollateralized loans – collateralization ratios and liquidation mechanisms will be largely in line with what you will find on those platforms. The key difference is that where Aave/Compound offer open-ended terms at a variable rate, we will be enabling fixed-terms at fixed-rates. In TradFi, both the floating rate and fixed rate markets are inextricably linked. In an efficient market, fixed-rates should be equal to the geometric mean floating rate over the same period of measurement. If it weren’t so, there would exist arbitrage opportunities that ultimately bring those two markets back in line. In this way, fixed-rate and floating rates are two sides of the same coin. Whether users choose one or the other primarily depends on their asset-liability needs. For those who have floating rate liabilities/assets, they will prefer floating rate borrowing/lending. For those that have fixed liabilities/assets (e.g. rent, expenses, income etc.), they may find that fixed-rate fixed-term borrowing/lending is a better match.

Fixed rates are a central pillar of Term Finance. What is your market outlook for fixed vs variable interest rates? Why have fixed interest rates not become a DeFi standard (yet)?

While fixed rates have not yet gained much adoption in DeFi, that is not to say that it has not gained adoption in crypto as a whole. In Q2 of last year, Genesis and Galaxy Digital originated >$80bn in fixed rate loans backed by digital assets in a single quarter. This far exceeds the combined TVL on floating rate lending in DeFi over the same period. All of the fixed rate borrowing/lending was happening offchain in the CeFi world. With the fall of Genesis, clients are re-evaluating the wisdom of leaving collateral in the trust of unregulated black box CeFi institutions. We believe that going forward, with the tailwinds of the lessons learned in 2022 that DeFi fixed-rate lending will catch steam. One of the key blockers to fixed-rate lending in DeFi has been the inability of existing AMM models to scale to the institutional size required by the large crypto institutions. We believe that our auction model solves this problem.

Will Term Finance become a DeFi primitive for the lending space and/or interest rate protocols?

Using auctions to match borrowers and lenders on a fixed-rate basis unlocks a few key items for DeFi. First, because auctions do not require standing idle liquidity (like in the AMM model) it is more capital efficient. Liquidity fragmentation is not a major concern. Term will be able to hold auctions on a weekly basis to build out loans that mature every week/month going out to, say, one-year. Second, by building out reference points for every duration out to one-year will serve as a key benchmark yield-curve for DeFi natives. These are reference rates that can be used for other interest rate protocols and for pricing other similarly dated uncollateralized/undercollateralized loans in the DeFi space.

In how far is Term differentiated from novel lending protocols like Morpho?

To my knowledge, Morpho is not an auction mechanism per se, but they do employ a matching mechanism. Morpho focuses on and serves as an intermediary between open-ended variable rate lending protocols (like Compound/Aave). Because loans on these protocols are open ended, Morpho can engage in asynchronous matching of borrowers and lenders. Funds can sit in Aave/Compound while they “wait” and as better opportunities arrive to the protocol, those offsetting users can be matched at a better rate than the Aave/Compound supply/earn rates. Asynchronous matching of borrowers and lenders, however, is not possible with fixed-rate fixed-term loans (borrowers and lenders must start and end at the same time by definition) the Morpho mechanism could not be applied to the fixed-rate market. We solve this problem by holding weekly auctions announced in advance to batch liquidity at single points in time via auction.

Governance is a huge discussion point for lending protocols. How is Term approaching this topic? Do you see best practices at other protocols?

Our focus in the short-term is heads down building of the protocol. Governance, if any, will become more relevant as we find product-market-fit. We do see many areas, however, where governance could be net positive to the protocol.

As the money market space has rapidly evolved over the last few years with both incumbent and new protocols, which opportunity in DeFi lending excites you the most?

The strength (and weakness) of DeFi lending is its anonymous and decentralized nature. This decentralized and anonymous character of DeFi is antithetical to unsecured/uncollateralized borrowing. It’s hard to track down someone whom you don’t know. For this reason, DeFi lending has had much more success with variants collateralized by digital assets – a relatively small world in the big scheme of things. As more real world assets (RWAs) come on chain, this should broaden the scope of DeFi lending in a manner that opens opportunities but stays true to the need for security in a decentralized and anonymous world.

What’s your customer acquisition strategy in the current market environment?

We’re focusing on a two-pronged approach. The first prong is general market education, through socials, podcasts and other media channels such as yourself. The second prong is through more traditional business development methods, e.g. one-on-one calls to potential users the old-fashioned way.

Do you think DeFi lending will eventually become a winner-takes-all-market with one big platform having >80% of the market?

The answer to this depends on how you define the DeFi lending market. If you group all DeFi lending variants into one (floating rate, fixed rate, secured, unsecured, open-ended, fixed term etc. etc.) then no. But if you look at the major subcategories of DeFi lending I do believe that each subcategory will be dominated by one or two large platforms having the majority of the market share within its respective group.

Risk management is a crucial ingredient for protocol success in DeFi lending, but it is often underrated. What risk factors should users look at when using Term Finance?

Collateralized borrowing has been around for centuries and its principles are well known. Users should focus on (i) what is the collateralization ratio? (ii) how liquid is the underlying collateral (iii) how quickly does the underlying collateral move (iv) is the collateralize ratio enough to cover black swan events? (iv) how is the market price of the collateral determined? (v) are the arbiters of market price trustworthy or is it vulnerable to manipulation? and lastly (vi) how is the collateral managed and what are the smart contract risks?

Oracle-free lending protocols is a new trend that founders jump on. Is Term opting for standard oracle-based liquidations or are you pioneering novel mechanisms?

We have pioneered many innovations to the standard oracle-based liquidation model but are not deviating in our V1 from this tried-and-true model from Aave/Compound. Very few protocols survived the bear market of 2022 but Aave and Compound did so handily and it is in large part due to their conservative collateralization ratios and instant oracle-based liquidations.

You will deploy on ETH Mainnet first. Do you have a multi-chain strategy on the roadmap and if so, what factors drive the decision for new chains?

We definitely plan to expand to other EVM chains. Our focus will initially be on chains with prominent and liquid native tokens (e.g. MATIC, BNB, ARB etc.) where we expect there to be a pre-existing market to borrow and lend those native tokens.