crvUSD launches on Mainnet, It's GHO-time for Aave, Memecoins are all the rage on Ethereum and Bitcoin, Q&A with Seraphim,...

crvUSD launches on Mainnet, It's GHO-time for Aave, Memecoins are all the rage on Ethereum and Bitcoin, Q&A with Seraphim,...

Issue #39 of The State of DeFi Lending newsletter

Welcome to issue #39 of The State of DeFi Lending, a newsletter covering the highlights of lending markets in DeFi.

In this issue we cover:

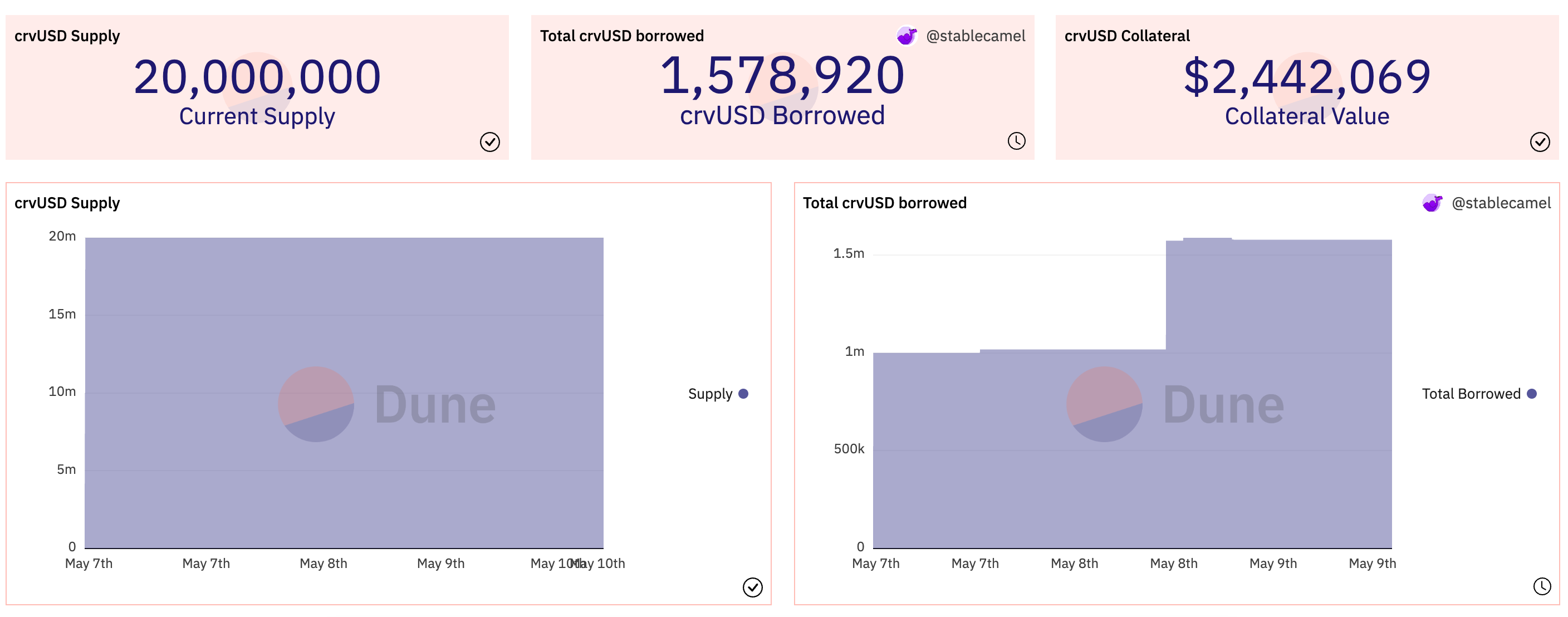

Curve Finance launches its stablecoin crvUSD which sets to distinguish itself through a wider collateral pool and less volatile liquidation mechanism. So far 1.6m crvUSD have been minted.

Following in Curve’s footsteps, the Aave DAO has been polling its community on the preferred direction for its GHO stablecoin. Key parameters like interest rate and debt ceiling have been voted on. In addition, the DAO is setting up the formal application process to become a Facilitator to mint/burn GHO.

Memecoins are sucking all the air out of crypto at the moment with heavy trading activity taking place both on ETH Mainnet and the Bitcoin blockchain. As a consequence, the number of transactions and fees are at yearly highs.

Seraphim, formerly Head of Risk at Euler Finance, sat down with us to share his thoughts on major trends in DeFi Lending.

Read below for more…

Please note: Twitter-links are not displayed as usual. Substack and Twitter are fighting out who has the upper hand in newsletter subscriptions. We hope to revert to the usual format as soon as possible.

News

Curve Finance has released its long-awaited stablecoin crvUSD and deployed contracts on ETH Mainnet. The first 1m crvUSD are backed by Frax’s sfrxETH.

https://twitter.com/WinterSoldierxz/status/1653949421594492928?utm_source=substack&utm_medium=email

So far, $1.6m in crvUSD have been borrowed backed by collateral worth $2.4m. The debt ceiling amounts to $20m.

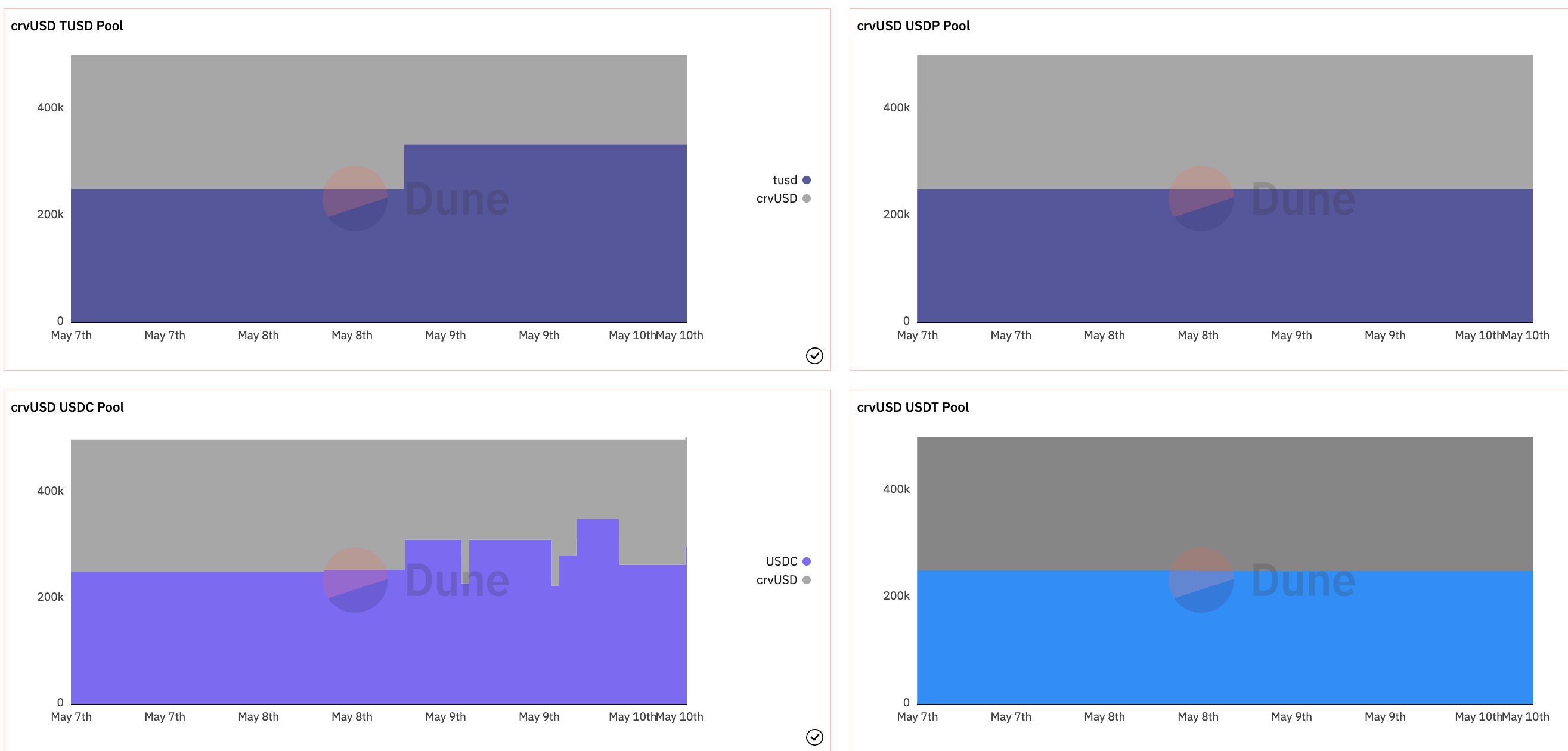

There are four crvUSD pools, paired with TUSD, USDC, USDP and USDT.

There’s only about 19 crvUSD holders so far suggesting the initial traction is due to some larger accounts testing out the stablecoin.

As a reminder of how crvUSD aims to differentiate: There is a mechanism called LLAMMA (short for lending liquidity AMM algorithm): If a user deposits $ETH to mint $crvUSD, the deposit gets transformed into an ETH/crvUSD LP position. If the $ETH price falls, the LP position sells some ETH and buys $crvUSD. This process is reversed if $ETH price rises again. This mechanism smooths out the volatility of the collateral to minimize liquidations.

We covered the crvUSD whitepaper publication in this newsletter in November last year.

The Curve team is testing in production and is teasing a UI to facilitate interaction with the protocol.

https://twitter.com/CurveFinance/status/1655933524187426819?s=20

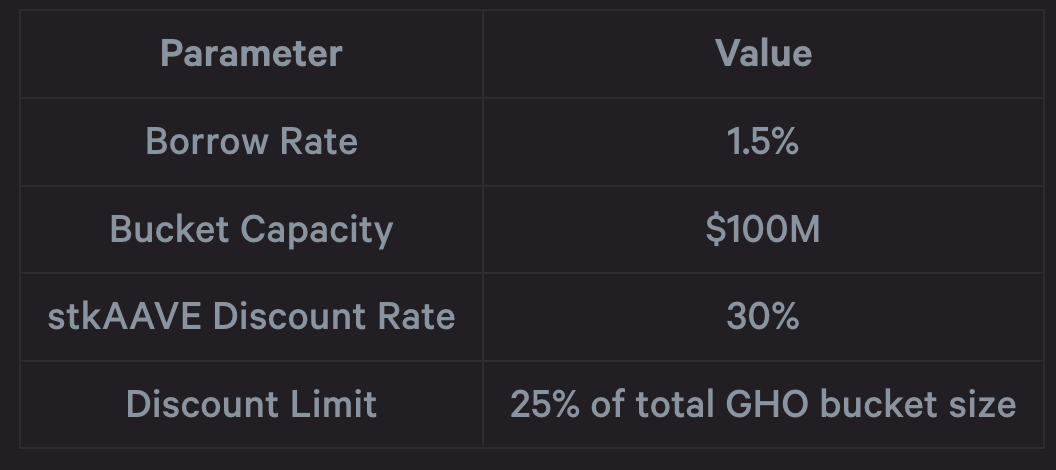

Aave’s stablecoin GHO is making further progress towards the launch phase as the community has voted in initial parameters.

GHO will launch with a debt ceiling of $100m, a borrow rate of 1.5%. $AAVE staker will get a 30% discount on the interest rate and the discount is limited to 25% of the GHO bucket size.

Aave also kicked off a request-for-comment to ratify the GHO Facilitator onboarding process. The onboarding process follows a relatively detailed format as Facilitators can trustlessly mint and burn GHO tokens. Hence, the community wants to make sure it selects appropriate Facilitators.

The entire application format can be found here. It has received overwhelming support in a Snapshot vote with 99.99% approval.

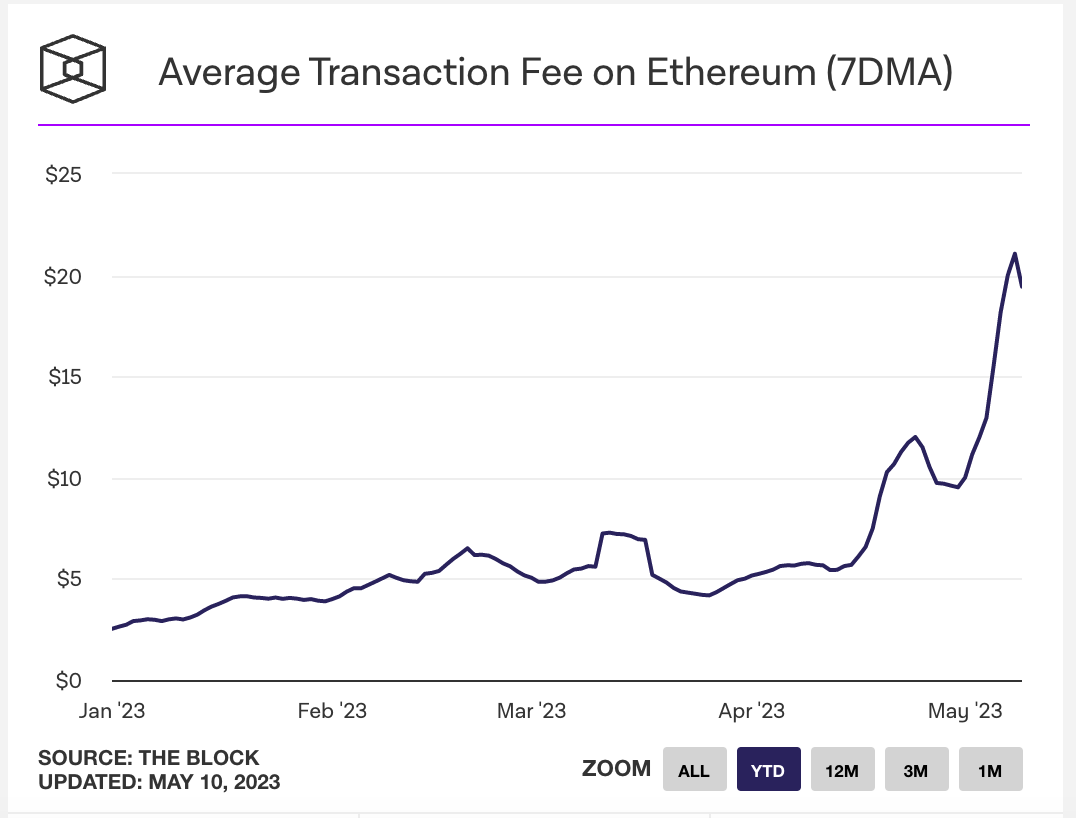

Memecoins are sucking all the air out of crypto markets at the moment as prices go up by several multiples. ETH Mainnet & Bitcoin transaction fees spike and generate significant fee revenues for validators/miners.

Traders have been flocking into memecoins, attracted by triple-digit APRs for LPing on Uniswap and eye-watering price action: $PEPE whose market cap peaked at $1B market cap, generated a 4,000% return from its price just 17 days earlier (per Coingecko data) .

The frenzy pushed average transaction fees on Ethereum to a new YTD high.

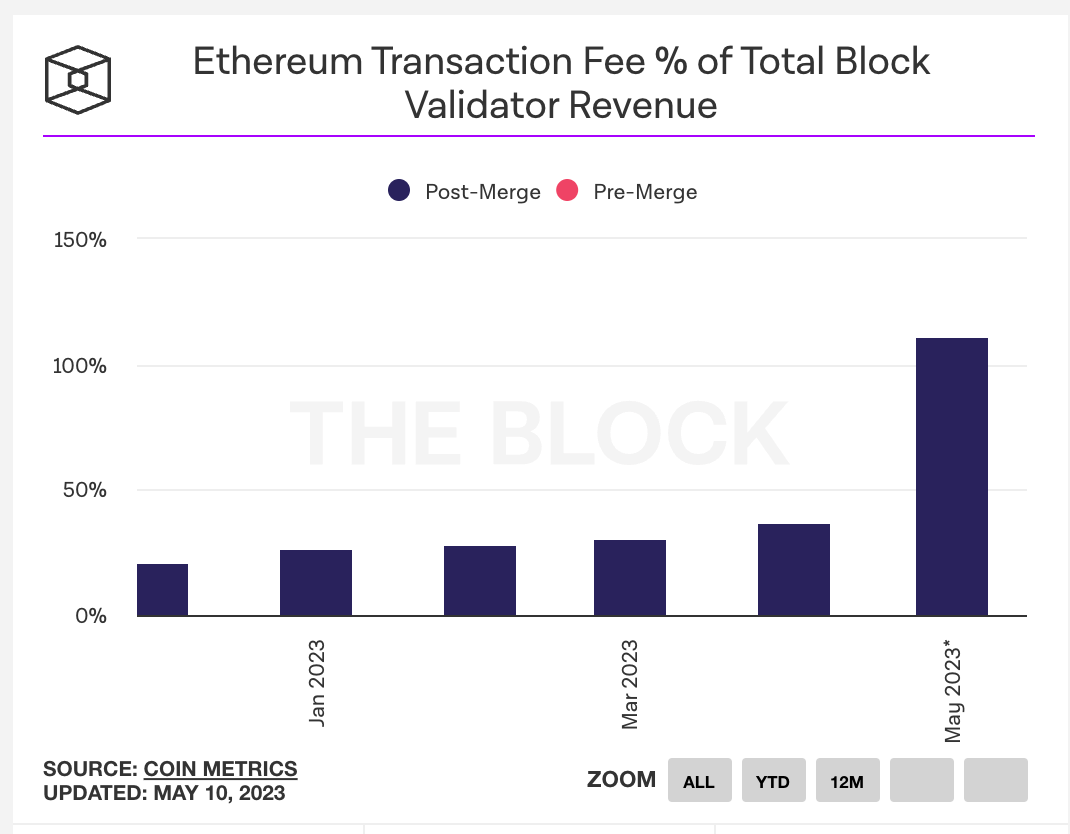

For the first time this year, ETH transaction fees are even higher than total block rewards.

The memecoin mania also pushed Uniswap users to new highs - not seen since May 2021 and contributed to significant MEV action. Jaredfromsubway.eth alone made $35m in profits from sandwich attacks since launching in February this year, according to Eigenphi.

The memecoin mania is also spilling over onto the Bitcoin ecosystem: The recent popularity of Ordinals Inscriptions and BRC-20 transactions pushed transaction fees on the Bitcoin chain to US$3.5 million on May 3, the highest since late May 2021.

Short news & announcements

Q&A with Seraphim

Seraphim, aka MacroMate8 on Twitter, is working on stETH growth in the BSC chain. Prior to that he was Head of Risk at Euler Finance.

As the money market space has rapidly evolved over the last few years with both incumbent and new protocols, which opportunity in DeFi lending excites you the most?

Personally I think looping Liquid Staking Tokens (LST) yield is one of the few real use-cases for lending protocols so far. Next is RWA, but that has regulatory hurdles.

Apart from that, looping on things like GLP is also exciting as it’s seems like a new asset class that has proven to generate real ETH yield.

Do you think that we will end up in a world where one lending platform controls most of the market, or will multiple platforms coexist?

At this point, it’s hard for lending protocols to differentiate themselves really. Aave v3 is pretty neat and does most of what a lending protocol should do, and it has all the liquidity. Most traders use other lending protocols simply to farm token rewards.

That might change though. There are many investment banks out there. But that’s also because they have achieved certain differentiation in terms of pricing they can provide in different products. Lending protocols don’t have that yet.

The topic of floating vs fixed rates has been discussed in this newsletter's Q&A section multiple times. What is your opinion on this subject? Do you think we will see more fixed-rate products in the future? Will lending protocols or external protocols that focus on interest rate swaps (e.g., IPOR) develop these products?

Sadly they’re not taking off and crypto just seems to love variable, which can be clearly seen in lending protocols and perps. So personally not too bullish until I see a clear use-case.

The best application I’ve seen so far was using Voltz to hedge ETH rates during the merge, as people were borrowing ETH to get forkedETH tokens.

Risk management is a crucial ingredient for protocol success in DeFi lending, but it is often underrated. Do you have any practical insights on teams that excel at risk management? What can other teams learn from them, and are there any useful resources available?

Euler risk framework was pretty good. I am obviously biased since I’ve built it, but the choice of collateral assets was very conservative: Stables, ETH and LSTs. The protocol did get hacked in the end, but it wasn’t related to the risk framework itself.

The reason why that choice made sense was that I recognised what traders wanted: To loop the yield on their LSTs. Everything else was redundant and increased risk.

New stablecoins are being announced almost weekly, but most backed-debt stablecoins have run into scaling issues. Do you believe that lending protocols and AMMs (e.g., Curve, Balancer) expanding into the stablecoin space will lead to the emergence of a dominant collateral-backed DeFi stablecoin?

I hope so, as it’s important we have a wider-choice of DeFi-backed stables. Incentivising liquidity in stables is an expensive game though, especially if your governance token has already been released. So eager to see if Aave and Curve can achieve that.

Some teams are working on novel liquidation mechanisms for DeFi protocols, such as insuring the collateral with ETH put options or making the loan similar to writing a covered call option (e.g., Myso Finance), where loan pricing becomes a function of option valuation. Do you think these protocols will gain significant traction, or will they remain niche products?

It all depends on the liquidity of the underlying products. Put options are neat but there needs to be a liquid market that can’t be easily manipulated to liquidate a user. I think as the market grows and products become more liquid, there will be traction. But before that liquidity is built up, it will probably remain niche.

The NFT Finance (NFTfi, and now Blend) space has recently gained significant momentum, with new protocols launching and loans being originated. What do you think is the sweet spot for NFTfi to grow into a meaningful DeFi primitive?

I think NFT perps are defo fun. They need to provide users with flexibility and leverage for them to be appealing. When it comes NFT p2p lending I am not so sure given p2p has never really properly taken off. But I would rather be bullish on the guys at Blur than not, so it’s not a strongly held opinion.