Curve exploit impact on DeFi lending, BProtocol launches SmartLTV on testnet, MakerDAO's EDSR is live, DAO governance in DeFi lending,...

Curve exploit impact on DeFi lending, BProtocol launches SmartLTV on testnet, MakerDAO's EDSR is live, DAO governance in DeFi lending,...

Issue #48 of The State of DeFi Lending newsletter

Welcome to issue #48 of The State of DeFi Lending, a newsletter covering the highlights of lending markets in DeFi.

In this issue we cover:

The last few days were an absolute roller coaster ride for DeFi lending, triggered by a Curve hack due to a Compiler issue in the Vyper code.

BProtocol launches Smart LTV on Sepolia testnet. The product is a suite of automated risk management tools for DeFi lending protocols.

MakerDAO’s EDSR is live. It allows DAI holder to earn up to 8% but decreases the higher the utilization rate is. It’s an innovative user acquisition strategy by MakerDAO which hopes to increase the circulating DAI supply.

DAO Governance in DeFi Lending is in the spotlight after the Curve situation. There’s an emerging debate about the elements that should be actively influenced by protocol governance, and how automated risk management can mitigate excessive risk accumulation in the future. This is a theme that will cause more discussion going forward.

Read below for more…

News

The recent hack of 5 Curve pools due to a Vyper compiler issue triggered substantial impact across DeFi lending. To summarize the series of events:

30 July: Curve gets hacked and funds worth $70m were drained from 5 pools (JPEG’d’s pETH-ETH, Alchemix’s alETH-ETH pool, the CRV/ETH pool twice, Pendle’s pETH-ETH pool, and Metronome’s msETH-ETH pool).

Chief among these hacked pools was the CRV/ETH pool that included 7m CRV tokens. As Curve was trying to contain damage from the hack, the market sold off CRV tokens as everyone expected the hacker to swap into ETH or stablecoins. CRV even wicked down to 8cts but no liquidations were triggered as Oracles take an average across several markets.

Curve’s founder Mich Egorov had outstanding loans worth $105m at the time of the hack, all secured on CRV collateral. Liquidation prices were around $0.4, a level that was within reach after the hack given the limited onchain liquidity for CRV.

In a frenzied effort to contain the second-order effects of the hack across all of DeFi, Egorov decided to sell CRV tokens OTC to reduce his debt balance. Tokens were traded for 40cts with a 6 months lock-up. To date, he has sold 144m CRV worth $57.5m.

Subsequently, Egorov partially repaid the loans, improving the health factor and reducing the liquidation prices even further (to less than $0.4). You can see his wallet profile on Debank here.

In the meantime, a number of stolen tokens were recovered from MEV bots or returned by the hacker. The Curve team offered a $1.9m reward (~10% of remaining missing tokens) to the hacker which has now turned into a bounty as the hacker did not accept the offer. The hacker even mocked Curve about his actions.

CRV price has recovered back to $0.6 which takes the heat off the situation. However, the urgency to resolve the outstanding loan situation is far from over and likely will continue for weeks to come.

There are also a number of second-order effects impacting DeFi lending at large:

Fraxlend’s interest rate model received major focus: At 100% utilization of a borrow-pair (users can only borrow FRAX), the interest rate doubles every 12hrs leading to exponential increases in Egorov’s interest liability.

Abracadabra tried to force Egorov’s hand to repay the loans by changing the interest rate model through governance. However, this got voted down.

Aave had a community discussion about buying CRV with treasury USDT. The Aave security module received renewed attention regarding its effectiveness as the reserves are denominated in stkAave: Aave DAO would have to sell Aave tokens to repay bad debt. In a downward trending market, this basically adds more selling pressure.

In case you wondered what Mich Egorov needed the money for: He went mansion-shopping in Australia.

For additional reading:

Curve Finance (by LlamaRisk) & Vyperlang post-mortem

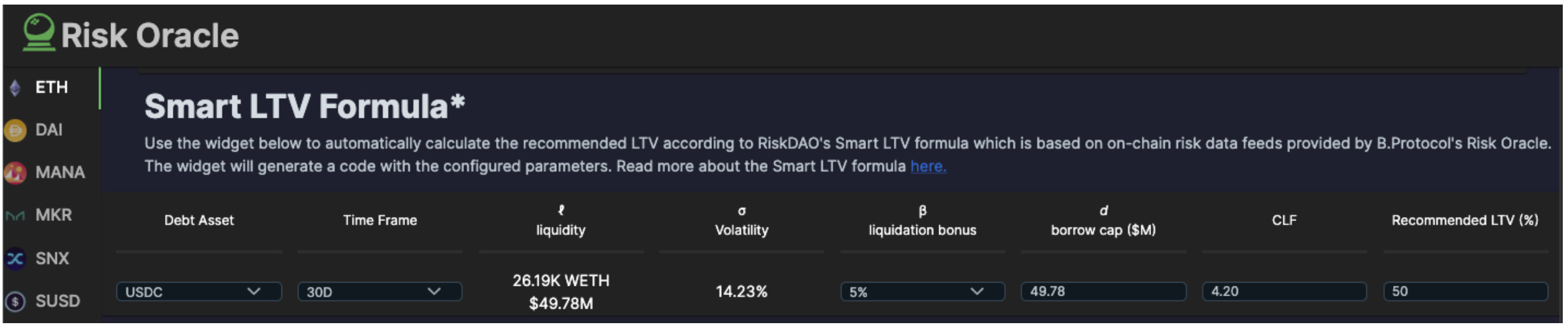

B.Protocol has launched SmartLTV on testnet. Utilizing the Risk Oracle, the SmartLTV formula provides a fully on-chain solution to calculate Loan-To-Value (LTV) ratios for risk management in DeFi lending.

B.Protocol has been at the forefront of risk management tools for DeFi lending protocols since its inception. In collaboration with RiskDAO, B.Protocol has generated tremendous insights into risk factors impacting DeFi lending. Based on the work of recent months, the team has taken a significant step forward in shaping the concept of a Risk Oracle, of which Smart LTV is the first live feature.

By utilizing risk-related data feeds, SmartLTV aims to eliminate human biases and inefficiencies found in current economic risk management. Developed by RiskDAO, the formula considers several market parameters, such as price volatility and liquidity, to provide robust LTV calculations. A newly launched front end provides visualization and even generates solidity code that can be used to set LTVs in smart contracts.

Users can set parameters to calculate a desirable LTV for an asset or input a desirable LTV to calculate the Confidence Level Factor (CLF), representing their risk appetite.

It should be noted that the Risk Oracle is still using testnet data and is considered a proof of concept at this stage. B.Protocol intends to gradually decentralize the Risk Oracle with the support of validators and expand the list of supported assets.

A detailed write-up by B.Protocol can be found here.

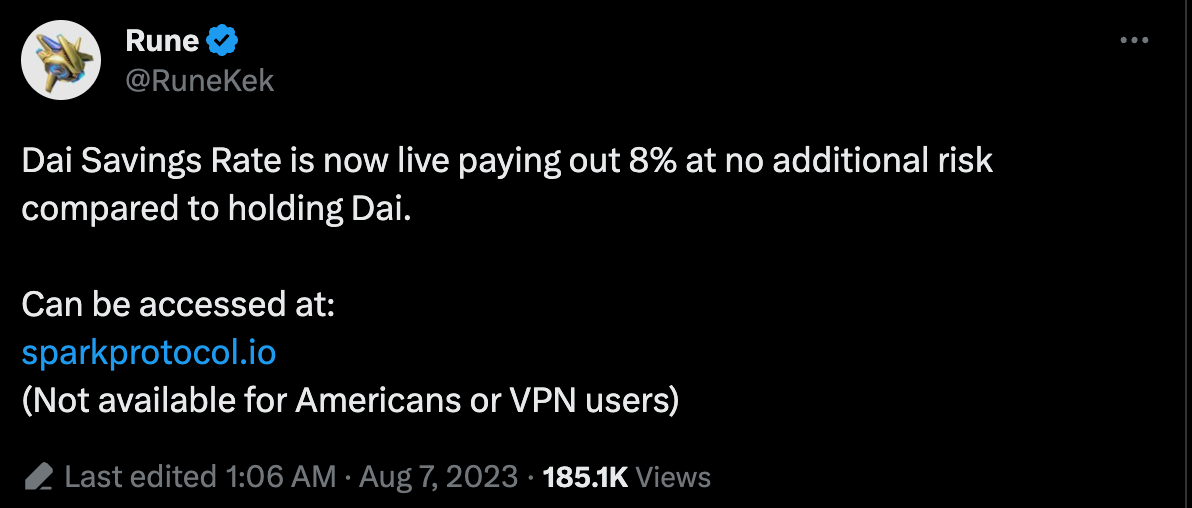

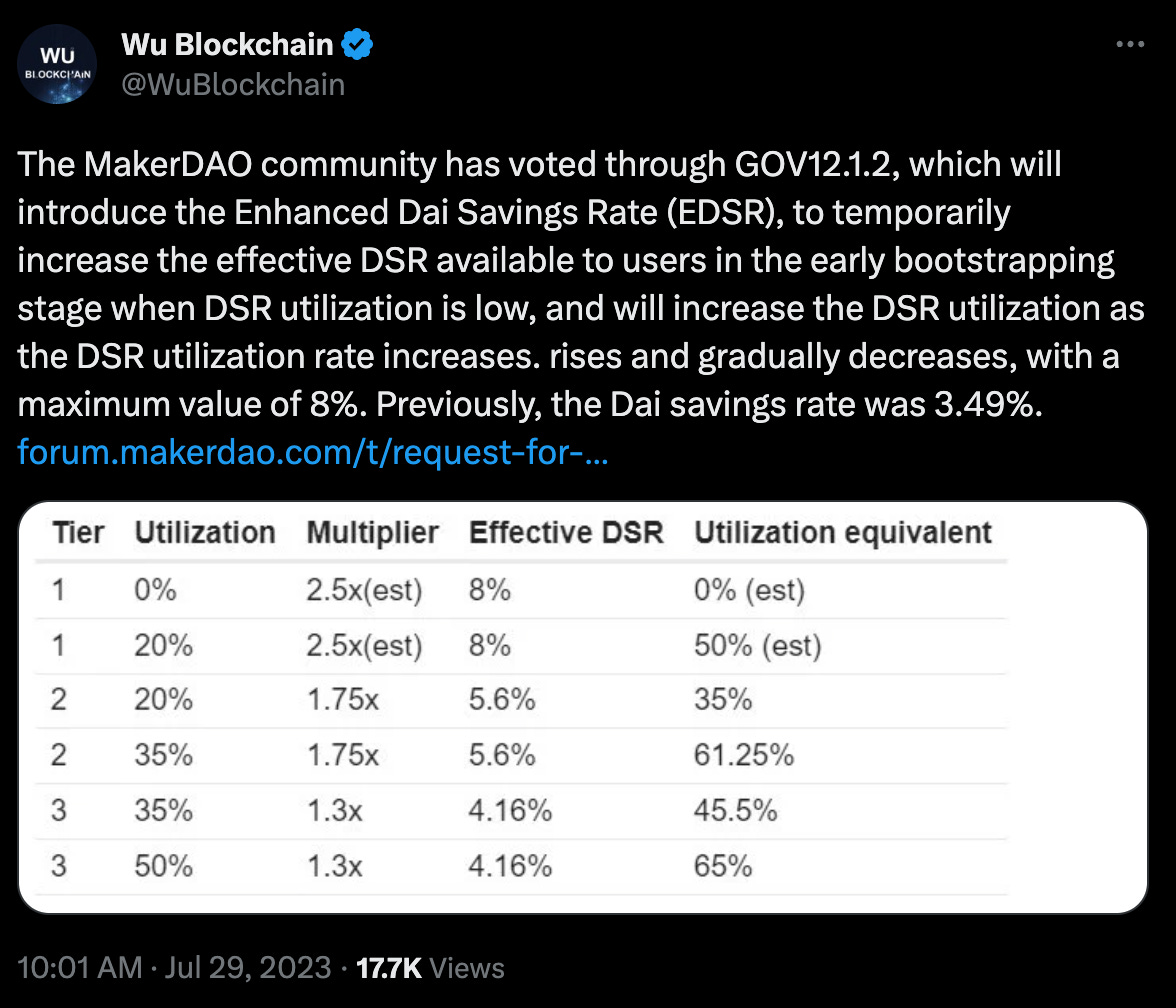

MakerDAO has voted in the Enhanced DAI Savings Rate (EDSR) in an attempt to increase adoption of the decentralised stablecoin.

MakerDAO activated the EDSR to temporarily increase the DSR when utilization is low, decreasing over time until it's eradicated at a pre-determined level.

The DSR increased from 1% to 3.49% in June, adjusted to 3.19% in July, and now sits at 8% following EDSR activation. Deposits in the DSR have reached $893m, equivalent to a 17.8% utilization.

The amount of DAI in circulation has declined drastically from ~7B to ~4B tokens since August 2022.

The ESDR is making its way through DeFi into other protocols:

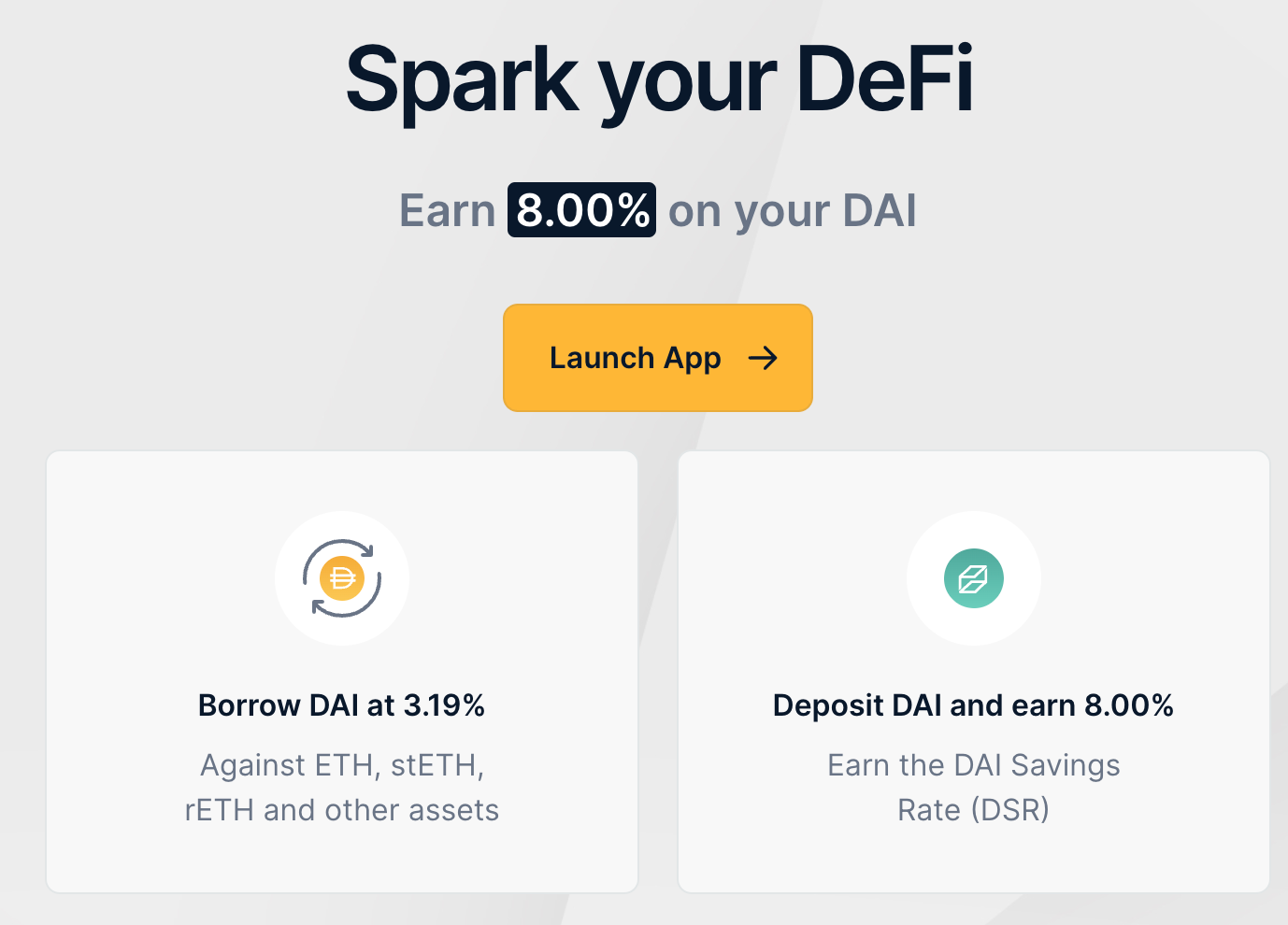

MakerDAO’s recently launched lending protocol Spark is offering a rate arbitrage opportunity whereby users can borrow DAI at 3.19% and reinvest into Savings DAI to earn the ESDR.

Source: sparkprotocol.io Interest rate swap protocol IPOR has incorporated the ESDR into their vaults, boosting yields for DAI deposits.

Cricism of the EDSR revolves primarily around the extra cost to MakerDAO. However, others highlight that the additional minting of DAI leads to inflows to MakerDAO which can be invested into yield-generating RWAs. It is likely that utilization continues to go up pushing the DSR below 5%.

Last week’s events focused on CRV’s concentration risk across lending markets and has generated intense debate about governance and risk management in DeFi lending.

At it’s peak, close to 50% of CRV’s circulating supply was deposited as collateral on lending markets, mostly on Aave v2. At the same time, liquidity has diminished significantly in line with overall market dynamics. Any liquidation of CRV would have resulted in adverse price movements, potentially triggering liquidation cascades.

Also keep in mind that this CRV position had previously been attacked by Avi Eisenberg.

“In the wake of the Eisenerg exploit attempt, Aave governance voted nearly unanimously to pause borrowing of CRV while still allowing it to be used as collateral. Since then, Egorov’s CRV collateral position has grown by more than $100mn.” Source: Kaiko Research

Market observers quite rightly wonder how so much risk could accumulate on Aave v2. It seemed that risk parameters for CRV were set in 2021/22. This puts a big question mark around risk management and governance. Gauntlet posted a post-mortem on risk management actions for Aave v2.

However, teams are working on novel tools to automate risk management:

Previously mentioned B.Protocol’s Risk Oracle and SmartLTV: The SmartLTV accounts for onchain liquidity and would have raised red flags about CRV’s declining liquidity to adjust the LTV.

BlockAnalitca’s automated interest rate model: The proposed mechanism introduces a controller to the traditional IRMs. This adjusts the borrow rates to maintain optimal market utilization, automatically adapting to changes in equilibrium borrow rates without needing active governance.

B.Protocol hosted a Twitter Spaces shortly before the publication of this newsletter about “The Role of Governance in Lending Market’s Risk Management”. Make sure to check out the recording.