DeFi 1.0 token renaissance, TUSD confidence crisis intensifies, MakerDAO update, Midas Capital exploit,...

DeFi 1.0 token renaissance, TUSD confidence crisis intensifies, MakerDAO update, Midas Capital exploit,...

Issue #45 of The State of DeFi Lending newsletter

Welcome to issue #45 of The State of DeFi Lending, a newsletter covering the highlights of lending markets in DeFi.

In this issue we cover:

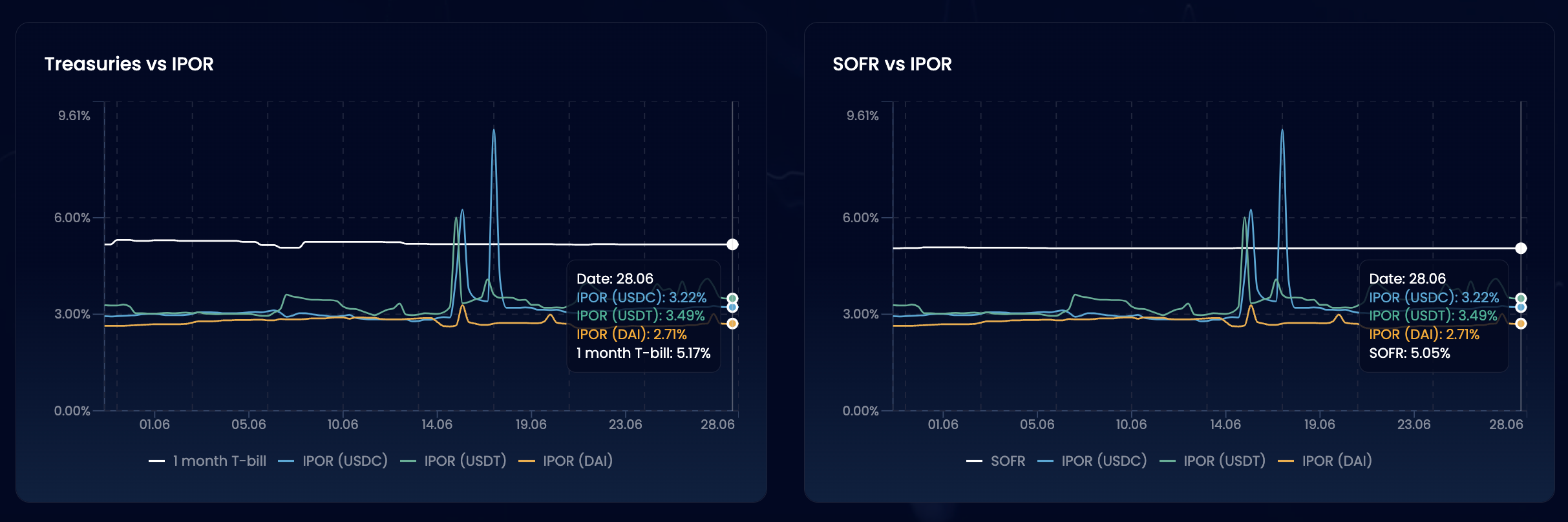

DeFi 1.0 tokens saw double-digit price gains over the weekend, leaving the market searching for suitable narratives. One thing is certain: OG lending protocols like Aave & Compound continue to attract TVL in spite of APRs that are below tradFi risk free rates.

The Prime Trust default triggered a confidence crisis around TUSD, a dollar-pegged stablecoin whose recent ascent has mostly been due to Binance’s TUSD adoption as a major trading pair. The stablecoin is under pressure as the market speculates on its peg resilience.

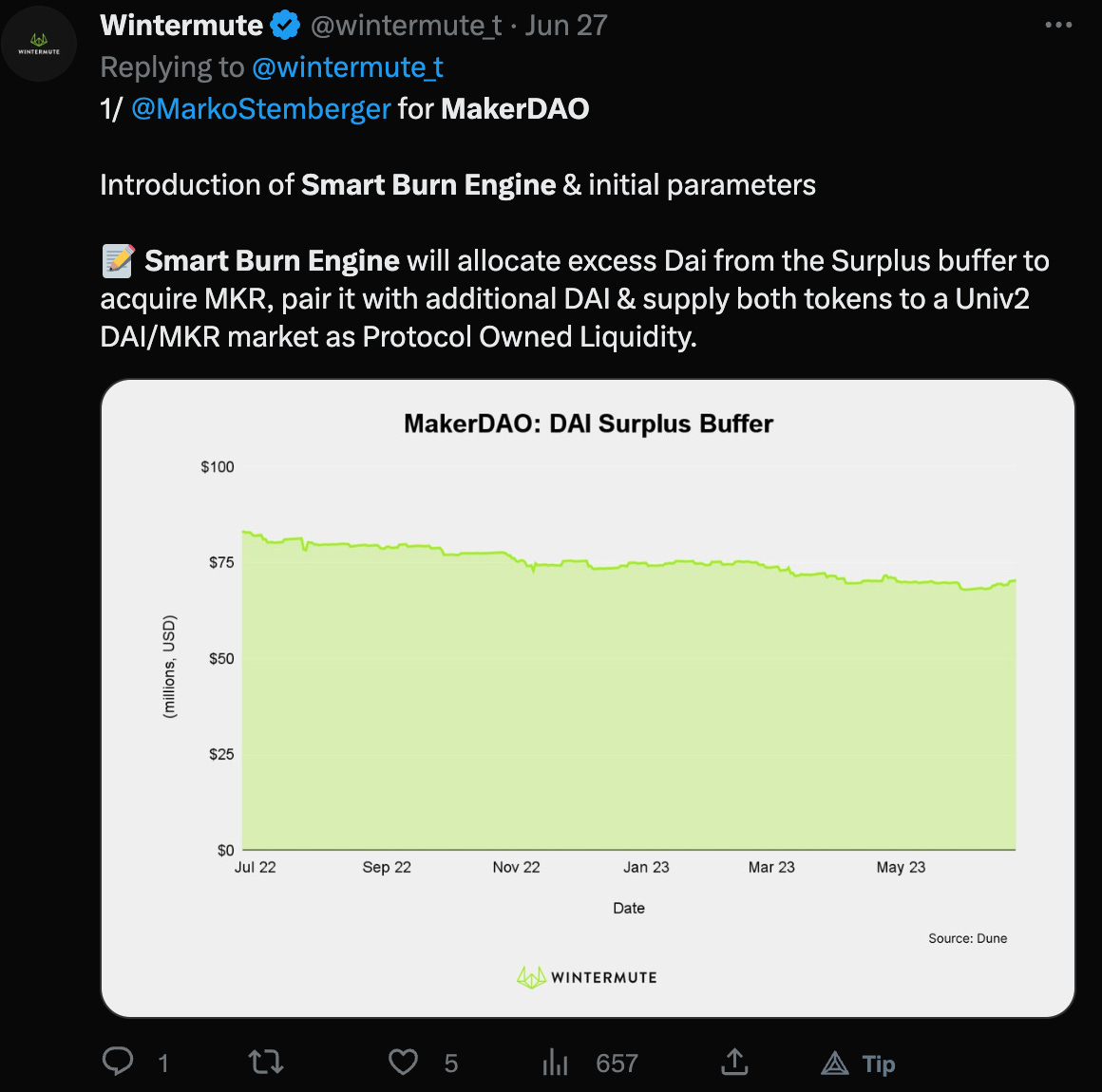

MakerDAO launched a smart burn engine to make use of its DAI surplus buffer: Reserves are earmarked to purchase MKR, pair with DAI and re-supply the MKR/DAI LP tokens to Uniswap. In other news, Maker has grown it’s exposure to RWAs from 2% to 41% since October 2022. Annualised fee income amounts to $118m for MakerDAO.

Midas Capital, a Compound-fork, got exploited for $600k in a hack that was similar to the one affecting Hundred Finance a few months ago. The exploit comes in spite of the team’s effort to fix the bug that impacted Hundred Finance.

Read below for more…

News

DeFi 1.0 token, including Aave & Compound, experienced a renaissance over the last weekend when prices rose double-digit (although nobody really knows why).

These double-digit price gains come on the back of strong absolute TVL changes for Compound and Aave (both v2 & v3).

Deposit and borrow rates remain subdue, especially when compared with tradFi risk free rates.

Token prices have already come down again leaving market commentators puzzled about who or what caused the pump. However, the significant TVL-increases in spite of low risk-adjusted rates begs the question whether LPs speculate on future upside from the GHO launch.

The Aave community is actively working on design parameters for GHO: This proposal suggests that all primary GHO pools should be launched on Balancer V2, explaining that BAL incentives will exceed the trading fee revenue generated on other DEXs.

The following happened in Aave risk-related news:

CRV market: The Aave community voted down a proposal by Gauntlet to freeze the Aave v2 CRV markets and set the LTV to nil. The proposal came in response to v2’s heavy exposure to CRV (285m CRV worth $190m) as a collateral asset. CRV’s market depth and liquidity have fallen substantially over the last months. Liquidations would cause substantial slippage that trigger more forced selling and potentially send the price into a death spiral.

TUSD markets: Gauntlet proposes to reduce the LTV for TUSD by 250bps or freeze the TUSD supply market entirely. TUSD has seen unusual activity on Aave which coincides with Prime Trust stopping minting of TUSD.

TUSD confidence crisis triggered by Prime Trust default

TrueUSD (TUSD), a dollar-pegged stablecoin managed by TrueUSD (a registered entity that belongs to TrueCoin LLC), recently stated that it had "no exposure" to the crypto services company Prime Trust, which is currently facing regulatory scrutiny. This statement comes in the wake of Prime Trust shutting off all fiat and crypto deposits and withdrawals following an order from state financial regulators.

TrueUSD reassured the market that they no longer use Prime Trust for minting or redeeming the TUSD stablecoin and maintain "multiple USD rails" elsewhere. Despite this, there has been some instability in the TUSD price, which has fluctuated between $0.995 and $1.003 since the start of Prime Trust's financial crisis on June 9. User are apparently not able to redeem TUSD.

In response to this volatility, the loan markets for TUSD, particularly on Aave v2 (the largest on-chain lending facility for TUSD), have experienced a shakeup. The variable borrow rate for TUSD has risen above 30% APR, with traders still betting that TUSD could "depeg" significantly. Notably, one trader made a multi-million dollar short on TUSD, borrowing $2 million in TUSD against $2.5 million in USDC collateral.

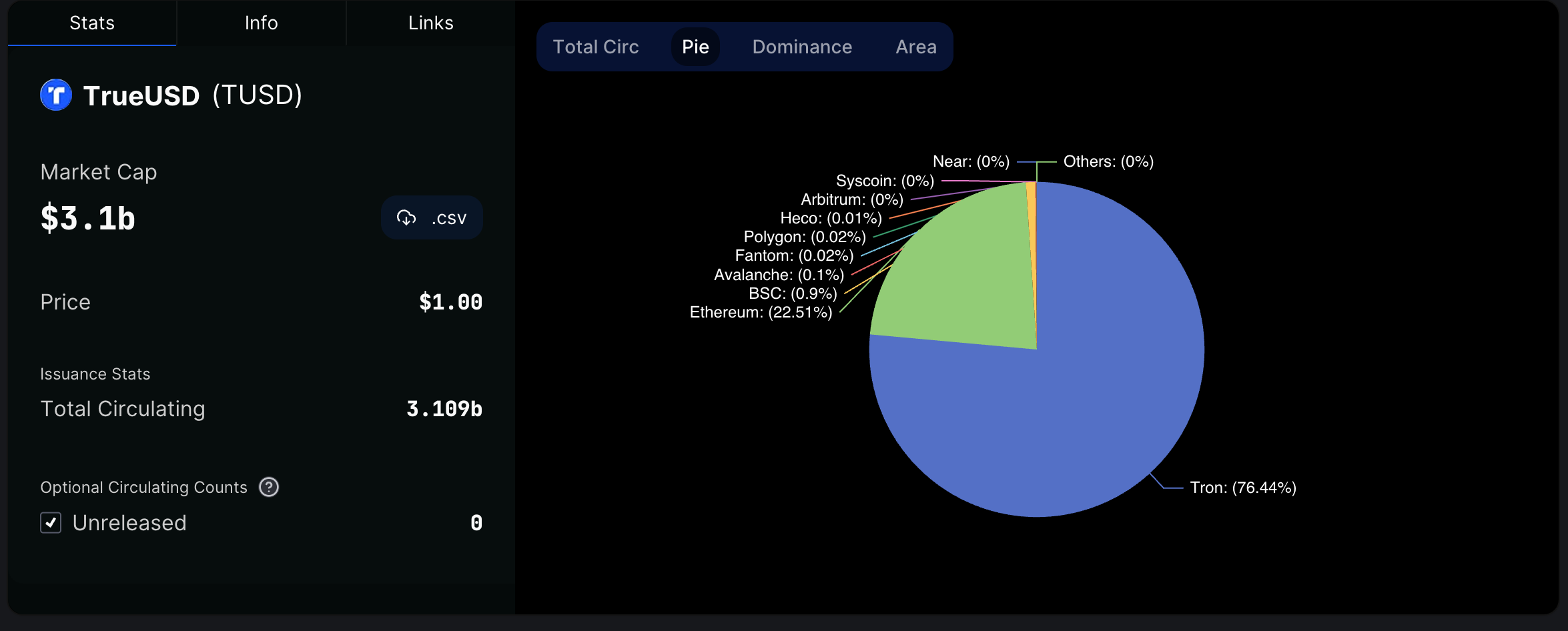

TUSD rose to prominence when Binance had to abandon BUSD and switched over to TUSD. TUSD become a major trading pair on Binance and tripled its market cap since the beginning of 2023.

TUSD is a Top 5 stablecoin by market cap and widely used on the Tron network. Its exposure on Ethereum is limited to ~$700m.

MakerDAO: Introduction of smart burn engine & growing exposure to RWAs

Smart Burn Engine: Unlocking the Potential of Surplus DAI

Maker has recently introduced the Smart Burn Engine, a smart contract system designed to allocate surplus DAI previously held as a contingency reserve. Instead of letting this asset idle, the Smart Burn Engine ensures improved capital efficiency.

What sets the Smart Burn Engine apart from the traditional burn design is its unique approach towards MKR tokens: The Smart Burn Engine combines MKR tokens with the surplus DAI. These tokens are sourced from the Uniswap V2 DAI/MKR pool and, when mixed with surplus DAI, are supplied back to the market. This action leads to an incremental but steady increase in the on-chain liquidity for MKR over time.

The DAI/MKR LP tokens created in the process are transferred to a protocol-owned address.

Increasing exposure to Real-World Assets

Since Q4 2022, Maker has reshaped its collateralization strategy, moving from a predominant reliance on stablecoins towards the increased use of RWAs.

This pivot has seen RWAs account for an impressive 41% of the collateral, with stablecoins making up around 30%. This is a substantial shift from early October 2022, where RWAs and stablecoins accounted for ~2% and ~64% of the collateral, respectively.

A deep dive into the composition of RWA collateral shows MIP65, managed by Monetalis Clydesdale, at its core. Focused on short-term Treasury bonds ETFs, MIP65 represents ~62% of all RWA collateral. Leveraging the current interest rate environment, Maker acquired $700 million worth of US Treasuries via MIP65.

By centering on RWA collateral, Maker has successfully scaled DAI issuance in the market and significantly grown its revenue. This financial boost has allowed for an increased DAI savings rate of ~3.5%, up from 1%. This adjusted rate, closely mirroring tradFi yield opportunities, could potentially trigger significant capital inflow into DAI.

The focus on RWAs is also helping Maker grow their fee income to $118m on an annualised basis.

Midas Capital, a Compound-fork, got exploited for $600k in a hack that was similar to the one affecting Hundred Finance a few months ago.

Midas Capital's isolated pool, supporting Ankr & Helio Finance, was exploited on June 17 when the attacker managed to circumvent a token's borrowing limit in a public, permissionless pool. A vulnerability was exploited which arose from a fix implemented after the Hundred Finance Hack, and was prevalent in cases with low-denomination LP tokens.

In response to this incident, Midas Capital is now refocusing its strategy on a more secure, permissioned design, allowing only whitelisted users to interact with the protocol.