Frax v2: a LST lending primitive, RiskDAO launches LTV index for lending markets , DeFi Interest rate derivatives' PMFit , MakerDAO's Endgame revisited, unshETH private key compromised,...

Frax v2: a LST lending primitive, RiskDAO launches LTV index for lending markets , DeFi Interest rate derivatives' PMFit , MakerDAO's Endgame revisited, unshETH private key compromised,...

Issue #43 of The State of DeFi Lending newsletter

Welcome to issue #43 of The State of DeFi Lending, a newsletter covering the highlights of lending markets in DeFi.

In this issue we cover:

Frax v2 positions the protocol as an LST lending primitive: Lenders put up ETH and the ETH stablecoin is backed by validator debt.

RiskDAO publishes optimised LTV framework for lending markets which uses a Uniswap-like formula to set LTVs and which is simple enough for a smart contract to compute.

Interest rate swaps and derivatives remain a niche product in DeFi to date. However, there are interesting innovations in the space that focus on yield-tranching for crypto-token which is generating sizeable interest.

MakerDAO keeps pushing the DeFi-boundaries and the Endgame is center-stage for the DAO’s future direction. We revisit some of the key premises of the Endgame.

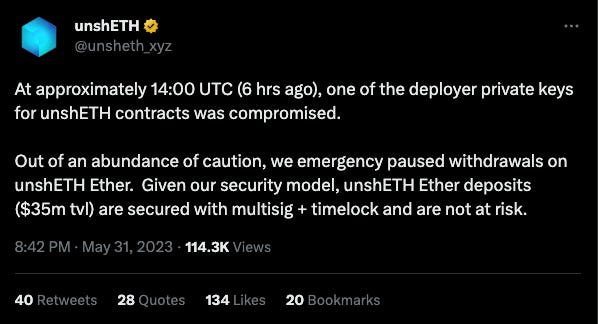

unshETH’s deployer private key was compromised and led to an emergency pause of the protocol. unshETH - a new LST stablecoin protocol - is still trying to negotiate a return of the assets with the hacker.

Read below for more…

News

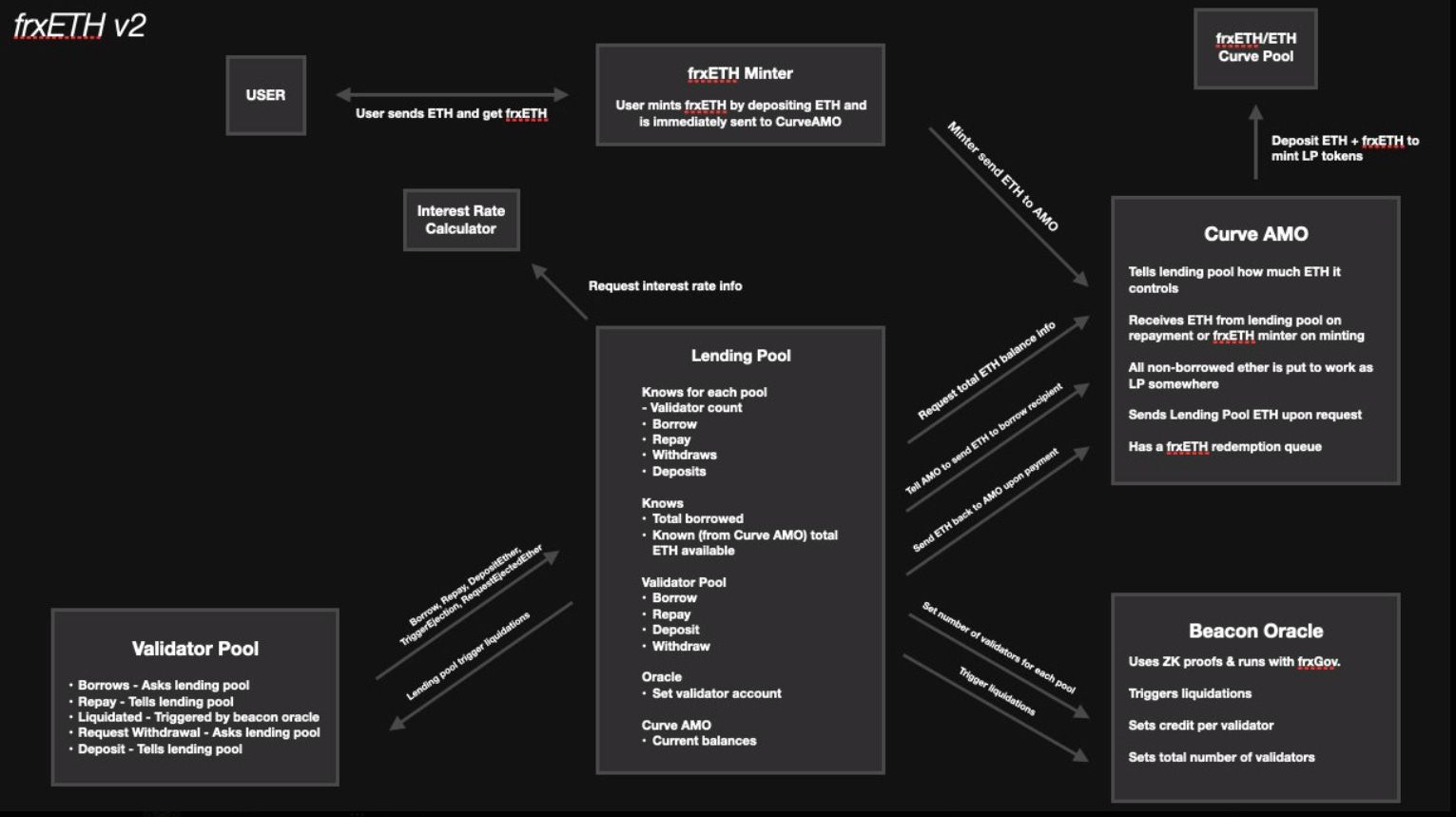

Frax’s Sam Kazemian introduces frxETH v2 as “the most efficient, decentralized lending market & ETH stablecoin backed by validator debt”.

According to Sam, the underlying structure of all LSD protocols are lending markets: Lenders lend ETH & get a receipt token (LSD). Borrowers rent the right to run a validator & pay interest to lenders.

Borrowers put up some ETH collateral & borrow a validator. Interest is paid directly from the ETH+PoS cash flow, just like in any lending market.

Interest rates are set by market forces & utilization rate. If it's cheap to borrow a validator, node operators can validate, pay the interest to lenders & keep the spread/MEV/tips etc. If interest rates spike & it's unprofitable to operate a node, a borrower simply ejects/repays the debt. The debt is in validators, not ETH.

Borrowers however have to monitor their LTV to avoid getting liquidated. If a borrower is slashed, the LTV rises & part of the collateral gets seized. If the collateral is getting close to not covering the debt, borrowers have to put up more collateral or risk getting liquidated.

Frax’s v2 will execute on this vision of lending markets for ETH & validator debt.

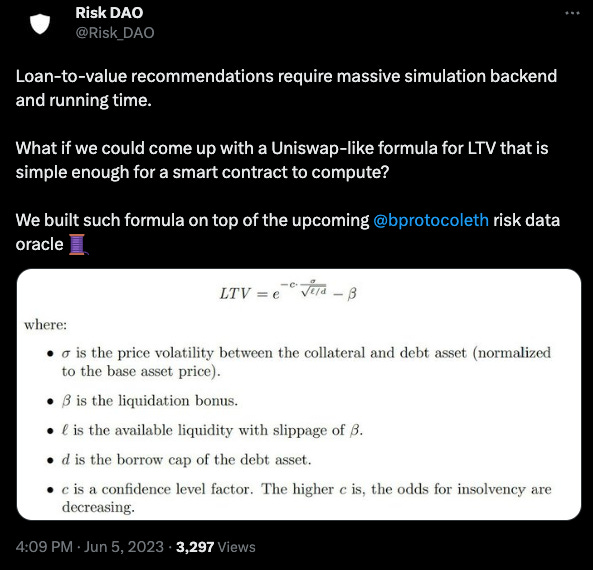

RiskDAO launched the LTV index that’s been the result of extensive risk modelling across DeFi. The formula was built on top of BProtocol’s risk data oracle.

To mitigate protocol bad debt risks, the traditional focus has been on the keeping Loan to Value (LTV) ratio under 1, but there might be a more efficient solution in the form of an adjustable confidence parameter (C).

This approach is designed to streamline smart security considerations and user behaviour assumptions into a single, easy-to-manipulate variable. By using this formula, market participants are not tied to a fixed LTV ratio; instead, they have the flexibility to determine the value of C, which can then automatically adjust the LTV ratio based on current market conditions.

The value of this approach can be seen in RiskDAO’s experimental results. The team analyzed data from Binance futures, focusing on price trajectory, liquidation times and sizes. The simulation of Decentralized Exchange (DEX) liquidity and liquidator behaviour provided insights into the maximum price drop of an open liquidation.

The results of the study clearly illustrate the potential benefits of using the adjustable confidence parameter:

With C in place, the LTV ratio is no longer a static, rigid figure. Instead, it becomes a dynamic, adaptable mechanism that adjusts to the ever-changing landscape of the market.

One additional advantage of this approach is its applicability for comparative analysis. The formula can also be employed as a ranking tool, offering a simplified method to assess and compare the risk associated with different platforms.

In conclusion, this innovative formula with the adjustable confidence parameter has the potential to transform the way we understand and manage the risks inherent in liquidation processes. You can find the entire report here.

Delphi Digital published a detailed report on the interest rate swaps space and looks into some of the more prominent protocols like Voltz, IPOR and Pendle.

We have covered interest rate swaps (IRS) in this newsletter at various occassions. You can read an interview with Carren from IPOR here.

It’s been a constant mystery to most observers why the IRS space has not taken off. Many blame the fact that most crypto-trader don’t want conservative and predictable - aka boring - yield but rather go higher up the risk curve. Other factors that mentioned are poor capital efficiency, impermanent loss and liquidity fragmentation.

In this context, the Delphi report also sheds light on some novel primitives such as Pendle which focuses on yield stripping. In Pendle’s v2, there are PTs (principal token) and YTs (yield token) which are traded in a single pool that consolidates liquidity and streamlines incentive accrual/distribution. Therefore, there is no need for separate liquidity pools which significantly reduces IL. Concentrated liquidity allows for increased capital efficiency and more control for LPs.

Pendle has seen a 5-fold TVL increase YTD highlighting the attractiveness to LPs.

In a market that is looking at outside stimuli for activity, having DeFi protocols that focus on native crypto yield could be a welcome boon to kick-start activity.

MakerDAO continues to be a major headline generator for this newsletter, given MakerDAO’s size ($6bn in TVL) and significance for DeFi lending. Much has happened with regards to the Endgame in the background and it is time to revisit some of co-founder Rune’s fundamental ideas about the future direction of MakerDAO.

In a recent interview, Rune Christensen gave insight into his plan to revolutionize DeFi. With the bold, five-phase transformation project named "Endgame", he plans to set the course of MakerDAO on the path of becoming a decentralized entity, free from the control of states and nefarious actors.

Christensen's mission is twofold: to protect Maker and DAI from potential adversaries such as governments and criminals, and to stimulate participation in the governance of MakerDAO. His focus is on resilience and mass-market adoption.

Major changes that are underway within MakerDAO are: Introduction of 'subDAOs' to manage governance, incentivizing voters in MakerDAO's decision-making process, and even rebranding Maker and its two tokens, DAI and MKR.

One of the significant changes involves the creation of 'subDAOs' or subsidiary DAOs to manage specific governance aspects. An example of this initiative's potential is the Spark Protocol, a service enabling Maker users to secure loans in DAI without a third-party intermediary. This new feature, expected to become a subDAO, has demonstrated what Maker could achieve by decentralising its operations further.

You can revisit our interview with Spark Protocol here.

Christensen’s vision also embraces the use of real-world assets, like stocks, bonds, and real estate, as collateral within the Maker ecosystem.

However, the transition has not been without its challenges. Some core engineers left in April due to ideological differences, and the anonymity requirement for delegates introduced recently may further impact the organization.

Whilst the Endgame preparation are underway, other developments within the MakerDAO ecosystem include:

BlockAnalitica publishes decentralised credit scoring tool for wallets with open MakerDAO vaults

DAI savings rate to increase to 3.49% and expected to go live on 12 June

Coinbase has successfully deployed 500 million DAI from the Coinbase Custody vault that will generate an estimated $13m in DAI annually

LST-backed stablecoins are all the rage in the current market environment as they promise substantial growth rates and attractive incentive models. One of the sector’s new darlings, unshETH, had a dramatic wake-up call last week as one of the deployer private keys was compromised.

The hack impacted $USH farm rewards and liquidity protocol to the tune of $375,000. The team was quick to avert any major damage and reinstated the protocol’s functionality within 48hours of the incident.

The security incident also impacted ancillary protocol contracts (eg bridges, farms) and the unshETH team is trying to negotiate with the hacker. As of 2nd June, the hacker returned the contract ownership but still retains the stolen $375,000.

Short news & announcements

Cat-in-a-box, a lending protocol for yield-bearing assets, launches a spinoff version of the protocol which offers boosted yields for maintaining riskier CDPs

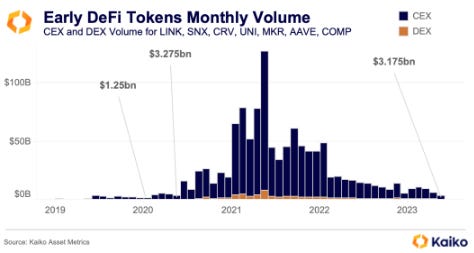

DeFi blue-chip tokens register lowest volume in 3 years, according to Kaiko Research. The combined CEX + DEX volume of LINK, SNX, CRV, MKR, UNI, AAVE, Comp fell to a low of $3.2bn, not seen since May 2020 right before the start of DeFi summer.