MakerDAO's Spark approves GNO collateral, Aave upgrade incident, crvUSD readies for mainstream, Tokenized bonds get a boost,...

MakerDAO's Spark approves GNO collateral, Aave upgrade incident, crvUSD readies for mainstream, Tokenized bonds get a boost,...

Issue #41 of The State of DeFi Lending newsletter

Welcome to issue #41 of The State of DeFi Lending, a newsletter covering the highlights of lending markets in DeFi.

In this issue we cover:

MakerDAO’s Spark Lend Protocol has adopted GNO as one of their first collateral assets as a way to deepen strategic ties between the two protocols and add native DAI liquidity to Gnosis Chain.

Aave’s Polygon-v2 deployment left users unable to access $120m in funds over the weekend due to an upgrade bug. However, no fund were at risk and a fix has been deployed.

crvUSD has finally launched it’s UI to enable mass-market access. Adoption has been muted so far with only $5m in circulating crvUSD. But crvUSD is “in production” and more upgrades are expected.

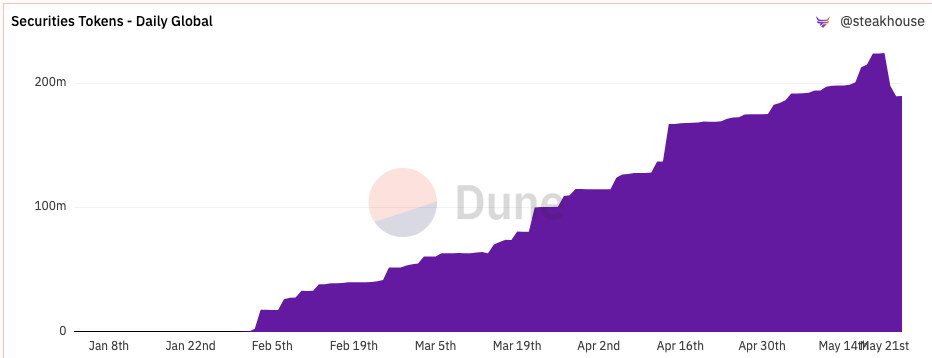

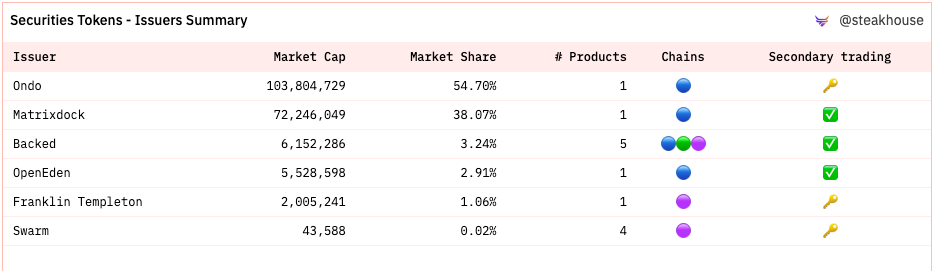

Real World Assets, most notably tokenized bonds and stocks, have seen strong performance YTD reaching an ATH market capitalization of $224m a few days ago. Ondo and Matrixdock are the leading the pack in terms of AUM.

Read below for more…

News

The MakerDAO community has voted in GNO as a collateral asset on the Spark Lend protocol.

https://twitter.com/MakerDAO/status/1658214705654292480?s=20

GNO will be added as a strategic collateral type, facilitating a credit line to GnosisDAO, which is expected to deepen DAI liquidity on the Gnosis Chain.

DAI is used natively on Gnosis Chain and GnosisDAO describes itself as “…one of the largest borrowers in Maker…”. Hence, this decision is seen as a strategic step to further cement ties between the two protocols.

https://twitter.com/karpatkey/status/1659138267772784640?s=20

Borrowing terms are restrictive with a debt ceiling of $5m and an LTV of 20%. As of writing, there’s ~$30m DAI on Gnosis which ranks the chain 8th by the amount of DAI. GNO has a FDV of $340m.

This initial “strategic alignment” seems to be a test-case for how well the collateral performs and if Gnosis Chain can generate active traction with more available DAI liquidity.

Users on Polygon-Aave v2 had temporarily lost access to approximately $120 million over the weekend due to a bug in a recent upgrade to the "ReserveInterestRateStrategy" contract.

https://twitter.com/BlockSecTeam/status/1659601021432365056?s=20

A legacy issue has led to a discrepancy between the Aave v2 versions used on Polygon (and Avalanche) and Ethereum, specifically related to the interface employed by the LendingPool to call an asset's rate strategy.

“The new interest rate strategies applied to those assets respect the interface of Aave v2 Ethereum, but not v2 Polygon, so when the LendingPool queries the strategy for the current rate, this call reverts, and so does the action “wrapping” it (e.g. deposit, borrow, etc).” - Source: Aave forum

The bug impacted assets such as USDT, BTC, ETH & MATIC. No assets were at risk and borrowers were able to top up collateral to maintain sound health factors.

The community was quick to respond in order to assuage users’s concerns and proposed a fix to Aave governance as the bug was discovered.

Curve Finance is readying its new stablecoin crvUSD for mass-market launch and finally launches UI.

crvUSD had been unaccessible for most users given the technical complexity to mint directly from the contract. The recent release of a UI should alleviate this problem.

Adoption of crvUSD so far has been muted with only $5m crvUSD borrowed and 41 holders. The collateral pool consists mostly of sfrxETH and amounts to ~$7m.

The Curve DAO is working on expanding the eligible collateral pool to include assets such as stETH. The delay in adding more tokens has been attributed to the fact that Curve is using proprietary oracles for crvUSD which require more time for testing.

This article from curve marketcap includes additional information on crvUSD, including some user guides.

In a market besieged by regulatory uncertainty and missing narratives, Real World Asset protocols have attracted significant attention recently.

The combined market cap of tokenized securities, specifically bonds and stocks, has reached an ATH of $224m only a few days ago. This number has been achieved within the last 4-5 months as most tokenized security protocols only launched at the beginning of the year.

Recent entrants like Ondo Finance’s OUSG and Matrixdock’s STBT tokenized products launched for investors only in January and attracted more than a combined $175m in assets. Both protocols tokenize short-term government bonds.

Investment giant Franklin Templeton's Franklin OnChain U.S. Government Money Fund (FOBXX), offering BENJI tokens, grew to $276 million in assets by April end.

Tokenization of real-world assets like government bonds is becoming a major trend in crypto, with strong interest from entities holding significant amounts of stablecoins.

The uptrend in RWA tokenization coincides with muted DeFi activity and depressed yields, offering investors alternative sources of risk-adjusted yield.