RWAs go on-chain, Aave updates, Compound's renaissance, risk factors to stETH's peg, Surge Finance's oracle-free lending mechanism,...

Issue #46 of The State of DeFi Lending newsletter

Welcome to issue #46 of The State of DeFi Lending, a newsletter covering the highlights of lending markets in DeFi.

In this issue we cover:

Real world assets (RWAs) are swiftly finding their way on-chain, prompted by early adopters such as MakerDAO and increasing TradFi yields. Protocols are rushing to tokenize risk-free rates and other cash flows from RWAs.

The last two weeks were particularly busy for Aave as the long-awaited GHO launch is about to happen. BGD is proposing a cross-chain messaging layer to turn Aave into a multi-chain ecosystem and there’s also been risk parameter updates for TUSD.

OG lending protocol Compound is experiencing a renaissance as TVL grows, the token price rallies and a new leadership team steps in. It’s all been prompted by Robert Leshner’s decision to resign and focus on a new RWA venture.

stETH has established itself as the leading LST collateral asset on lending protocols. It is primarily used for loop-borrowing between stETH and ETH to arbitrage the yield differential. This arbitrage trade however is based on a peg that’s relying on on-chain liquidity which appears less sticky than it used to.

Surge Finance launched recently on Arbitrum and is one of the novel, oracle-free lending protocols. Surge’s collateral ratio is determined by pool utilization instead of price, hoping to avoid price manipulation as an attack vector for long-tail lending markets.

Read below for more…

News

Real World Assets (RWAs) are the new kid on the block(chain)

RWAs are taking over DeFi. The number of recent announcements and launches has been phenomenal to say the least.

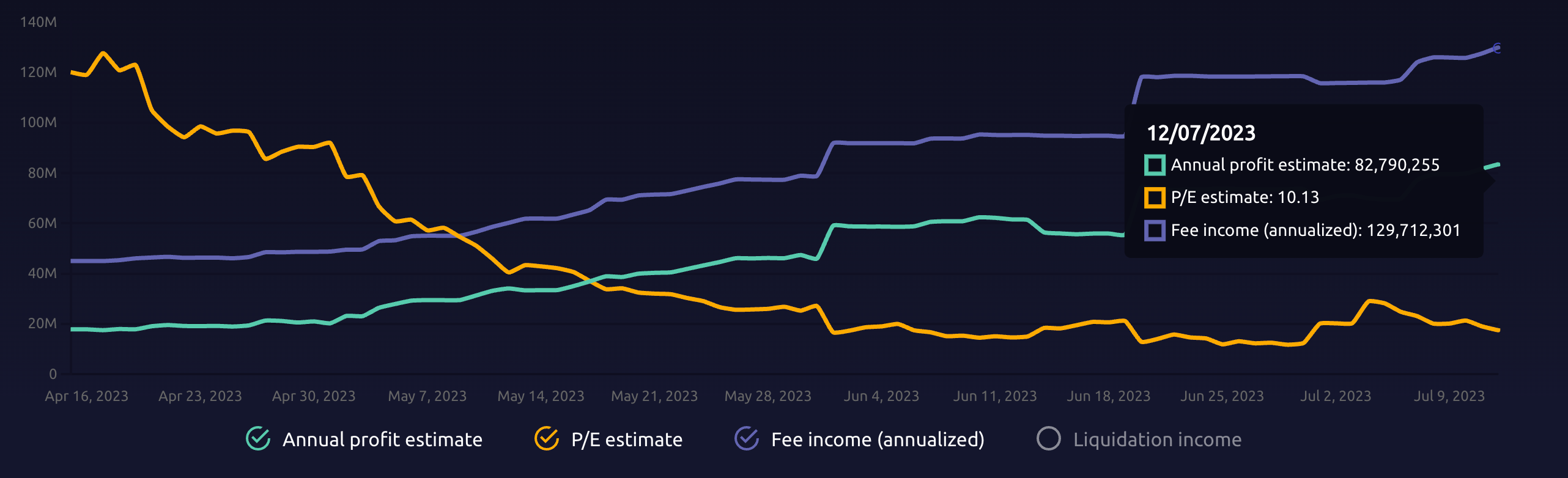

MakerDAO remains the #1 case study to understand how an RWA allocation strategy translates directly into earnings and indirectly into DeFi yields (via the DAI Savings Rate). Annualised fees and profits have been on a steady upward slope over the last 3 months amounting to $130m and $83m, respectively.

MakerDAO is publishing in-depth reports about their RWA strategy and allocation providing up-to-date transparency and accounting.

MakerDAO has been tokenizing US treasury yields indirectly. However, there has been a steady growth in direct UST yield tokenization amounting to ~$613m in on-chain TVL, yielding 4.2% on average. These funds are spread out across a range of products and protocols with each of them aiming to carve out their own niche.

RWA.xyz launched a new research report, shedding some light into the market landscape. It’s striking how tradFi & DeFi names are starting to overlap.

Beyond tokenized treasuries, lending protocols continue experimenting with new products. Maple Finance, one of the more established RWA protocols, has announced the launch of a lending pool that is targeting Web3 start-ups. Pools will be overcollateralized and depositors will be VCs, family offices, DAOs and HNWIs. Maple aims to fill a gap left open from the demise of CeFi lenders like BlockFi, Celsius and Genesis.

The more TradFi yields go on-chain, the more DeFi and TradFi yields should converge. Looking at the IPOR index, it appears strange that risk-free TradFi yields are so much higher than DeFi stablecoin yields.

Aave updates: GHO, TUSD and a.DI

GHO mainnet launch

It’s finally GHO-time! As previously mentioned in this newsletter, the Aave community has been gearing up for the protocol’s decentralised stablecoin launch. The Aave Improvement Proposal has gone live and so far has a resounding majority as support (vote ends on 14 July, 9:17pm UTC).

This proposal specifies a set of actions that would initiate GHO:

Deployment of GHO ERC20 and transfer control over the smart contract to the Aave DAO.

Listing of GHO as a borrowable asset in the Aave Protocol.

Enrollment of Aave V3 Ethereum Pool as the first Facilitator of GHO.

Deployment of GhoFlashMinter and enrollment as the second Facilitator of GHO.

Configuration of stkAAVE as discount token for GHO borrow rate.

Proposal to freeze TUSD on Aave v2

Following the uncertainties around TUSD, its murky relationship with Prime Trust and temporary depeg on Binance.US to 80cts, the Aave community voted to lower the liquidation threshold and LTV to 77.5% and 75%, respectively. The relevant community discussion can be found here.

Introducing a.DI: Aave Delivery Infrastructure

BoredGhostLabs published a forum post to introduce Aave’s own cross-chain communication layer, nicknamed “a.DI”

Presenting a.DI (Aave Delivery Infrastructure), a cross-chain communication abstraction layer for a decentralized system like the Aave DAO to communicate across networks, minimizing the risk of any underlying bridge providers.

a.DI aims to reduce trust in underlying bridges, bolster security, improve development experiences, and allow adaptability for various cross-chain communication needs. Aave has continuously expanded across chains and the proposal aims to shore up Aave’s position as an ecosystem, rather than just a dApp.

Renaissance of DeFi lending OG protocol Compound

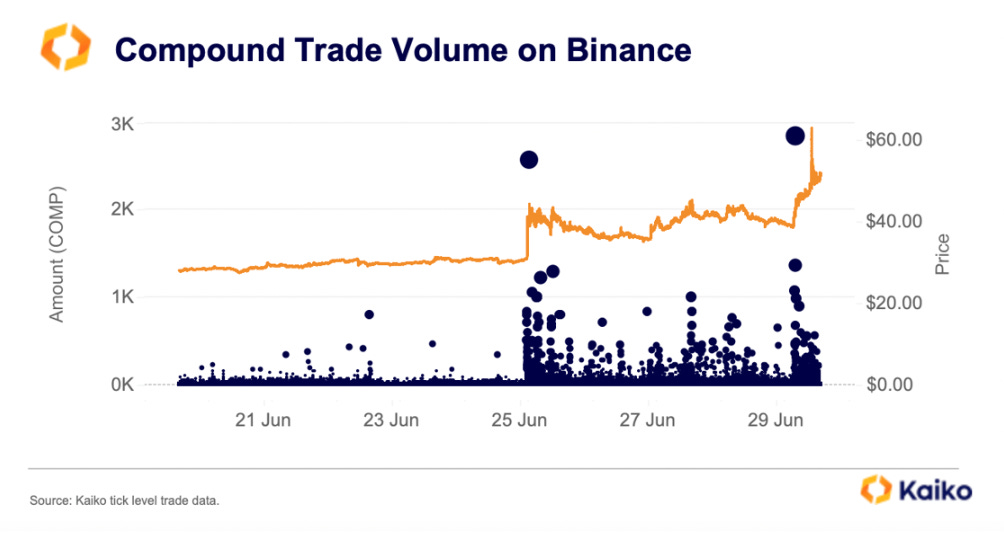

COMP has been one of the best-performing tokens as it registered a 150% gain over the last 30 days, even outpacing ETH by a wide margin.

It’s not entirely clear what has caused this sudden price pump but market observers noticed some whale activity across spot markets.

Compound’s founder Robert Leshner made headlines when he announced his resignation from Compound to focus on his new start-up SuperState Fund which focuses on tokenised US treasury bonds.

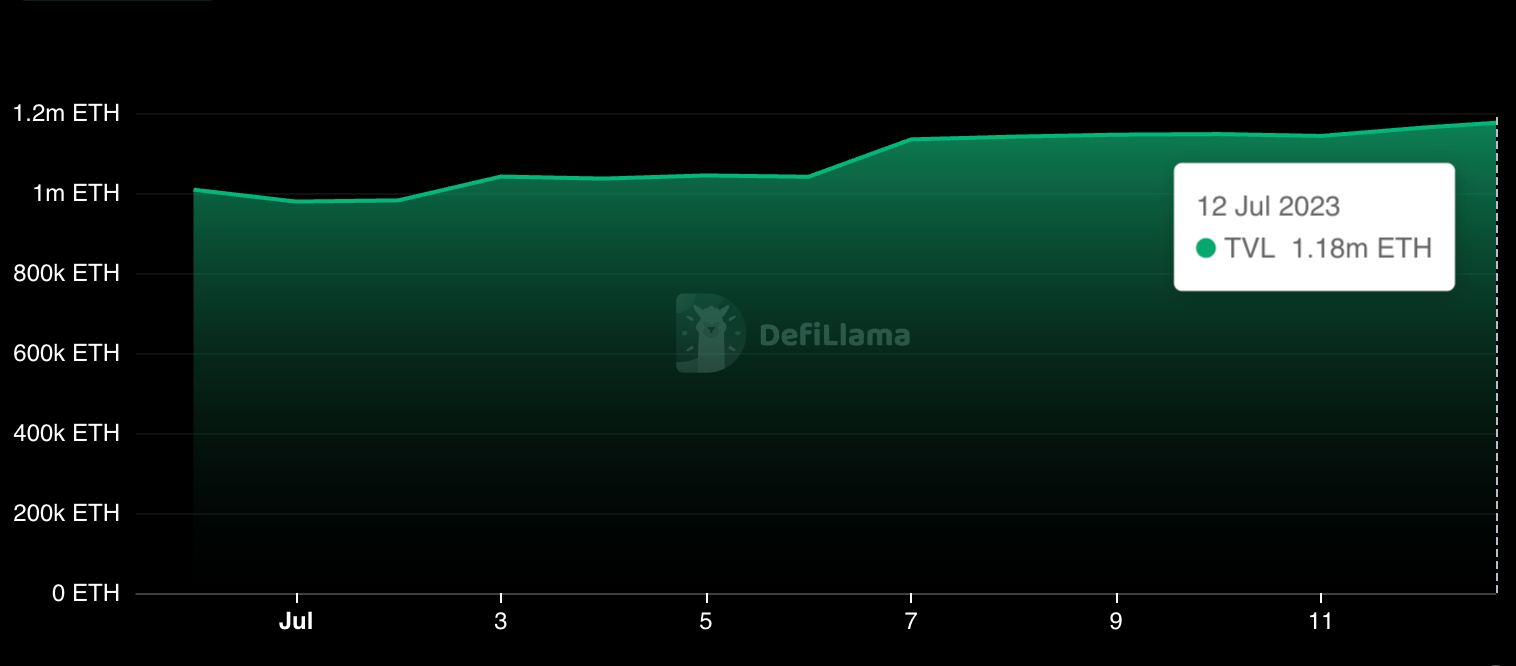

Compound’s ETH-denominated TVL has grown from ETH1m to 1.18m since the announcement. USD-denominated TVL jumped from $1.87bn to $2.2bn in the same time period. LPs and investors are turning more bullish on Compound’s future under a new leadership team.

stETH’s rise across DeFi lending markets and potential risks

Kaiko’s research team published an in-depth guide into stETH, covering on- & off-chain liquidity as well as stETH’s role for lending markets.

stETH has grown into a major DeFi collateral asset across lending protocols: There’s now more stETH deposited on Aave v2 + v3 than Curve. This trend has been reinforced by users’ loop-borrowing ETH for stETH to arbitrage the yield differential.

DeFi collateral assets require sticky liquidity for liquidations in case prices decline rapidly. The higher an asset’s lending TVL, the deeper and stickier on-chain liquidity needs to be to cushion liquidation cascades.

Lido DAO bootstrapped stETH-ETH liquidity on Curve through generous $LDO incentives (2.5m LDO as of Dec 2022) which have been entirely eliminated in June this year. The removal of LP incentives in combination with general market developments have led to a deterioration of on-chain liquidity.

The Shapella upgrade allows redemptions of stETH for ETH but there are certain nuances to it:

The problem with relying on ETH withdrawals is the time delay; according to Lido a withdrawal can take 1-5 days under “normal circumstances” and takes longer during periods of high demand. It’s easy to imagine a scenario in which liquidity continues to dry up in Curve, a market event (like FTX’s crash or USDC’s depeg) causes even more liquidity to be removed, the withdrawal queue lengthens, and stETH holders want to swap into ETH, leading stETH to fall relative to ETH.

stETH liquidity on ByBit and Curve were almost equal last week highlighting that off-chain liquidity is catching up, even though CEX numbers remain hard to verify.

It remains essential for DeFi lending protocols to properly underwrite the liquidity risks associated with stETH. Whilst a depeg appears a low probability event on paper, the reality shows that on-chain liquidity developments are not supporting stETH’s growing usage as collateral asset.

Launch of Surge Finance as one of the first oracle-free lending protocols

Surge Finance is a new lending protocol that launched recently on Arbitrum: The protocol treats liquidations as a function of liquidity rather than price.

Surge is made for long-tail assets and accepts any token as collateral since there is no reliance on external price feeds for liquidations. To determine liquidation points, Surge instead uses an algorithmic collateral ratio. The collateral ratio begins to decrease over time when a pool’s utilization hits a predefined “surge threshold”, which forces borrowers to deposit more collateral or return their borrowed funds to avoid liquidation. When the utilization rate returns below the surge threshold as a result of these actions, the pool enters a recovery state and the collateral ratio begins to slowly increase back to its default value.

The design is supposed to protect lenders and the protocol from oracle manipulation. However, lenders still need to monitor prices to determine when to pull liquidity and protect themselves from bad debt.

Surge uses an isolated pair model similar to Silo Finance to ensure lenders can base their liquidity decisions on a specific asset pair rather than across a cross-margined account. Surge allows users to create lending pools with any token pair and its code cannot be upgraded. Each pool comes with a fee switch that Surge can choose to activate in the future to collect up to 20% of all interest accrued to a pool’s lenders.

Short news & announcements

Thanks for reading The State of DeFi Lending! Subscribe for free to receive new posts as they are published.