Venus Protocol starts liquidating BNB collateral, DAO governance in risk management, Thorchain launches lending product, MakerDAO reduces EDSR to 5% and teases SPK airdrop,...

Venus Protocol starts liquidating BNB collateral, DAO governance in risk management, Thorchain launches lending product, MakerDAO reduces EDSR to 5% and teases SPK airdrop,...

Issue #49 of The State of DeFi Lending newsletter

Welcome to issue #49 of The State of DeFi Lending, a newsletter covering the highlights of lending markets in DeFi.

In this issue we cover:

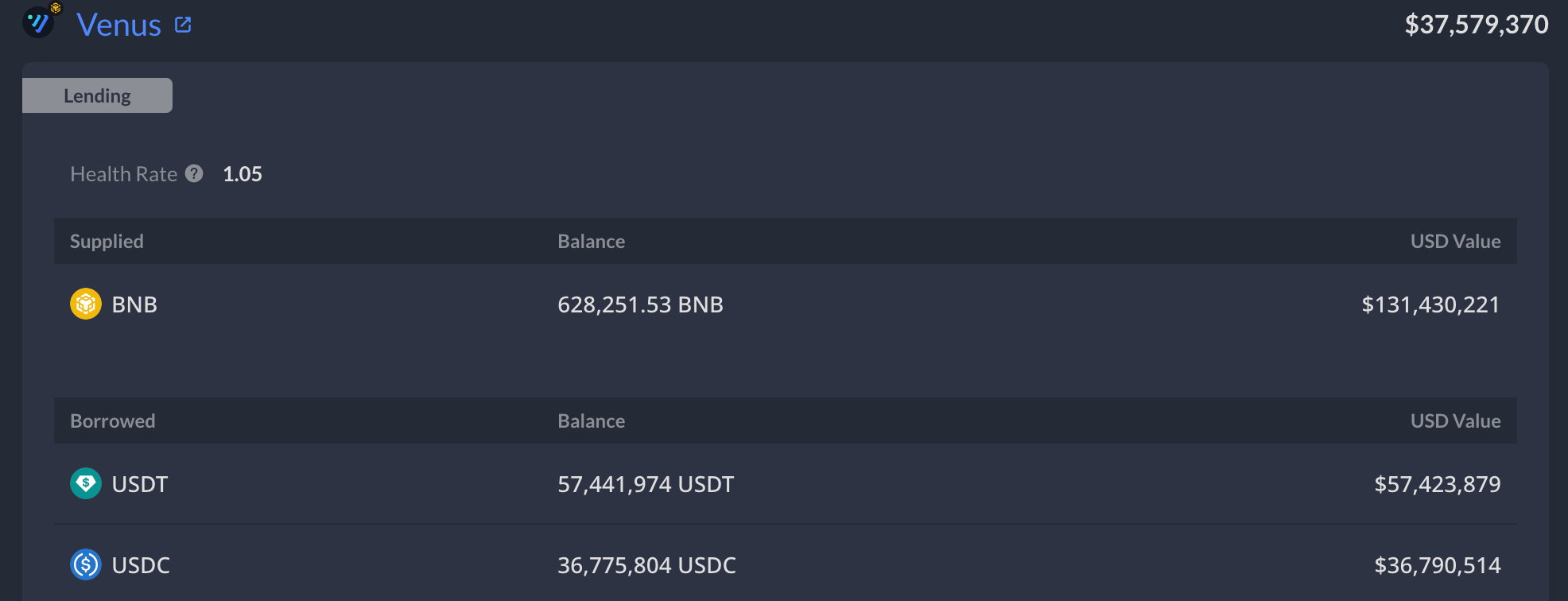

Venus starts liquidating BNB tokens which secure a $150m loan facility. The 900k BNB were deposited into Venus as a result of a cross-chain bridge hack and served as the hacker’s exit liquidity. As the market tumbles, BNB hit liquidation prices and liquidations are being executed by the BNB core team in its role as whitelisted liquidator.

Risk management continues to dominate headlines with many DeFi devs/contributors debating the Pros & Cons of DAO-governance.

Thorchain launches lending primitive: It comes with a zero interest rate, no liquidations or external oracles. BTC & ETH are the first two collateral assets at launch.

MakerDAO has voted to reduce the EDSR from 8% to 5% to contain whale games. MakerDAO is also teasing a retroactive airdrop of SPK token for those users that interact with Spark Protocol after the EDSR amendment.

Read below for more…

News

Venus Protocol starts liquidating a $150m loan position, collateralized by BNB tokens. The collateral ended up on the protocol as a result of a cross-chain bridge hack after which the hacker used Venus Protocol for exit liquidity.

These liquidations are backstopped by the core BNB team in an attempt to mitigate the sell pressure of cascading liquidations.

These BNB tokens found their way to Venus Protocol in October 2022 after a hacker capitalized on a vulnerability related to the “iavl hash check” within the BNB Chain's bridge, and the weakness allowed the attacker to mint 2 million BNB tokens valued at $560m at the time of the exploit.

Instead of selling and risking a price crash for BNB, the hacker collateralized 900k BNB on Venus to get a $150m stablecoin loan. They moved most of these stablecoins to other chains and exchanged them for ETH, likely without any intention of repaying the loan.

Due to the significant size of this loan, the BNB core team became the sole liquidator for the position. Recently, the BNB price declined, prompting the liquidator to intervene, seizing around $33M in BNB collateral and $30M in USDT.

The updated liquidation price now sits at $190 (originally $220) which is only a 10% drawdown from current levels. There is still ~$95m in outstanding debt on Venus. The wallet overview can be found here.

Venus Protocol is no stranger to bad debt: As per the RiskDAO bad debt dashboard, the protocol has accrued $75m from insolvent accounts claiming the #1 spot.

Risk management has been gaining traction over the last weeks ever since the CRV saga. Several DeFi devs & contributors are taking to the CryptoTwitter stage to debate ideas on how to manage lending risks in DAO-governed protocols.

First up, there’s been a Twitter Spaces with a deep bench of experts on this topic. You can check out the full recording here.

Morpho’s Paul Frambot wrote up an interesting summary of how we ended up with the current DeFi lending designs and in what way a combination of DAOs and external risk managers creates substantial issues.

Ivangbi from Gearbox also shared his opinion on the subject matter: He puts into perspective that protocols look for product-market fit and need to adjust things in order to get there. In a competitive environment, protocols require mutability and this needs to be implemented through governance. Ivan questions whether a radically opposing mechanism design (ie oracle-free, governance-free) is the ideal solution for new start-up lending protocols.

Thorchain launches its new lending product: It comes without liquidations, external oracles or interest rates.

Cross-chain swap protocol Thorchain is expanding into lending, starting with BTC & ETH as collateral. Users lend their native L1 assets to Thorchain to borrow a USD-denominated debt with no liquidations, no interest, and no expiration.

Loans are overcollateralized with collateralization ratios (CR) ranging from 200%-500%. Debt is denominated in TOR, a USD equivalent. Debt can be repaid in any Thorchain-supported asset, including stablecoins.

Loans have a minimum period of 30 days. Borrowers can repay their debt at any time after 30 days and receive their collateral back. Partial repayments are possible, however the collateral is not released until debt is fully repaid.

Thorchain is a cross-chain protocol that utilizes native assets of the most popular L1s. The team announced to expand the eligible collateral pool to other assets such as BNB, BCH, LTC, ATOM, AVAX, DOGE.

The Thorchain lending design mimics other, novel DeFi lending primitives that abstract away maturities, liquidations & oracle risks as well as interest rates (eg Myso Finance who we interviewed in this newsletter or Ajna Finance come to mind). The pricing of these loans can be treated as an options contract as described in the below tweet.

The design of the entire Thorchain lending product goes beyond the scope of this newsletter but there is a detailed blog post for those who want to dive deeper. What stands out is that Thorchain did not start out as a lending protocol but rather expands into a new product category based on its core swaps protocol. It’s somewhat similar to how Curve has recently ventured into lending with its crvUSD stablecoin.

Thorchain’s lending vertical is also expected to improve pool depth for swaps and to burn RUNE tokens.

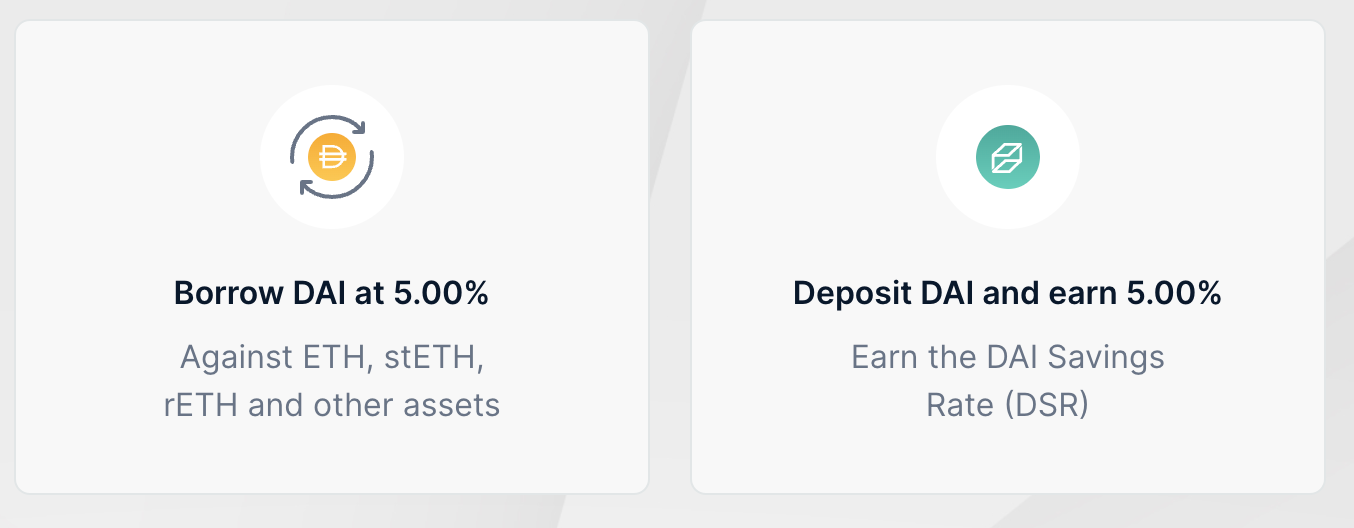

MakerDAO has voted to reduce the EDSR to 5% and teases an airdrop for Spark Protocol users in an attempt to reduce whale games and retain sticky liquidity on Spark.

Rune Christensen, MakerDAO co-founder, had proposed to reduce the EDSR from 8% to 5% which the MakerDAO community approved last week. The reason for this change was dissatisfaction with whale-heavy activity as described below.

“Overall, while in hindsight it is now obvious to me, I think the massive scale of ETH and Staked ETH whales harvesting yield from the EDSR through borrow arbing is unintended because it crowds out regular Dai users that the EDSR was supposed to primarily benefit, and I think we should act immediately to optimize the EDSR with this context in mind, to make sure it primarily benefits regular Dai holders.” - post by Rune Christensen in the MakerDAO forum

The motivation for the SPK prefarming airdrop is to encourage users and borrow-arbitrageurs to continue using Spark Protocol, especially after the 5% EDSR has taken effect. The objectives are to amass assets in the Spark Protocol, enhancing its reputation and trust, and to foster a dedicated community and DAO members for SparkDAO.

Borrowers using volatile assets as collateral will receive SPK tokens based on their borrowing quantity and duration. The distribution will resemble farming, with tokens airdropped collectively at the end.

Turning the focus back onto the EDSR: The elevated interest expense has burnt a hole in MakerDAO’s profit forecast. Annualized profits dropped from $84m to $4m after the EDSR started. After the recent adjustment, annualised profits have gone back up to $70m.

One can also observe that the EDSR led to a sudden spike in circulating DAI, jumping from $4.4bn to $5.5bn at its peak. The circulating supply has come down to $5.1bn ever since the recent changes.

Spark Protocol is in the center of the recent MakerDAO actions and the protocol saw a bumper performance over the summer: The DAI debt limit was hit less than two weeks after raising the ceiling from $20M to $200M. Maker noted that it only took eight days for users to borrow $180M DAI.

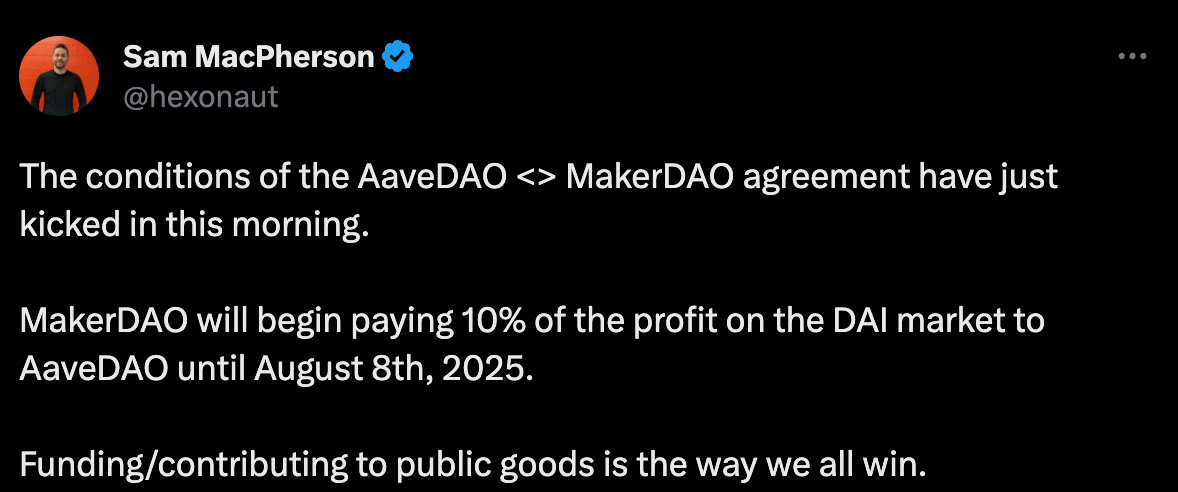

MakerDAO’s Spark Protocol - an Aave v3 fork - has commenced paying a 10% profit share to Aave as originally agreed between both protocols.

The DAI<>SDAI rate arbitrage has now disappeared as both rates stand at 5%.

Short news and announcements

IPOR - an Interest Rate Derivatives protocol - releases updated roadmap

Liquidations on 17 August spiked in the wake of slumping prices: There were over $62 million worth of liquidations on ETH Mainnet lending markets. This was the highest amount since the FTX collapse.

Maple Finance Eyes Asian Expansion With $5M Investment, Returns to Solana