Vesta Finance dissolves, Aave updates, Spark Protocol goes cross-chain, Maple Finance winds down undercollateralised lending as Goldfinch struggles with RWA loan default,...

Vesta Finance dissolves, Aave updates, Spark Protocol goes cross-chain, Maple Finance winds down undercollateralised lending as Goldfinch struggles with RWA loan default,...

Issue #52 of The State of DeFi Lending newsletter

Welcome to issue #52 of The State of DeFi Lending, a newsletter covering the highlights of lending markets in DeFi.

In this issue we cover:

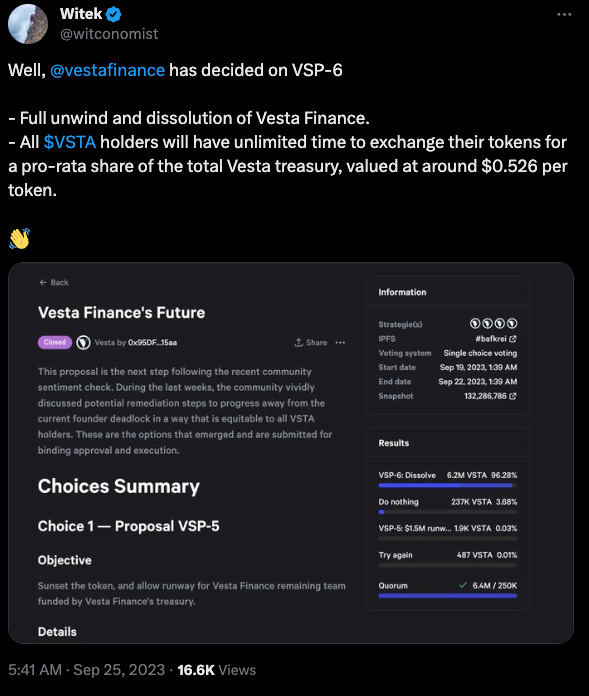

Vesta Finance will officially dissolve the project as per the most recent community vote. Tokenholder will receive ~$0.5 from the protocol treasury.

Aave’s community continues to tweak the GHO design to restore the peg. At the same time, the community is voting on lower payouts to the Safety Module staker and the DAO gets serious about RWAs by partnering with Centrifuge.

MakerDAO’s Spark Protocol is going cross-chain, most notably expanding to Gnosis Chain which uses DAI as their gas token. As Gnosis Chain increases transaction activity, DAI demand will grow alongside which is creating opportunities for Spark.

Maple Finance is withdrawing from undercollateralised lending, citing a lack of profitability and elevated risks. Goldfinch’s recent loan portfolio default (Tugende motor taxi company) is a prime example of the risk factors that undercollateralised lending exposes crypto investors to.

Read below for more…

News

Vesta Finance will dissolve as the community debated different paths for the lending market.

As covered in the previous edition of this newsletter, Vesta Finance will shut down and distribute its treasury. This came after two of the three co-founders suggested to rage-quit the project due to disagreements of Vesta’s future direction.

The next steps as per VSP-6 are:

Pausing the vesting contracts for team and advisors, and burning their unclaimable VSTA tokens.

Accelerating angel investors' vesting.

Burning all VSTA tokens owned by the treasury.

Withdrawing all Vesta-ETH protocol-owned liquidity.

Selling treasury assets (except for USDC and ARB) for USDC.

Deploying a redemption smart contract that allows users to burn 1 VSTA in exchange for a pro-rata share of USDC and ARB from the Vesta Finance treasury.

Developing a front-end to enable users to interact with the redemption smart contract.

Unlocking all VST in the stability pool.

Halting the minting of VST and only allowing the closing of positions.

Hosting front-ends for closing positions and redemptions on IPFS.

The VSTA token continues to trade at a discount to the dissolution payout as trading activity has come to a quasi-standstill.

Recent Aave ecosystem activities have centred on fixing the GHO depeg, adjusting rewards for the Safety Module as well as expanding into RWAs.

Finding a solution to the GHO USD-depeg

Aave's governance has decided to raise the borrowing rate of GHO from 1.5% to 2.5% to address its peg deviation and promote its market growth. Additionally, Aave is considering transitioning their stablecoin treasury assets to GHO.

There was a recent setback when Aave had to temporarily halt GHO due to a technical glitch. The investigation revealed that a user could exploit a rounding issue to repeatedly withdraw GHO tokens without affecting their position, potentially accessing GHO tokens up to the Aave Facilitator's capacity.

Aave plans to reduce its daily token emissions to the Safety Module (SM) from 1,100 AAVE to 770 AAVE, a 30% decrease. This will result in a drop in APR for stkAAVE holders from 6.87% to 4.81% and for those in the Balancer pool from 14.35% to 10.05%. The reasons for these changes include the introduction of new assets to the SM, a reduction in slashing by Aave, and a consensus that Aave has been overcompensating the SM.

Introducing Centrifuge as Aave’s RWA partner

Centrifuge becomes Aave’s RWA service provider and onboard part of Aave’s treasury to real-world assets, through the Centrifuge Prime platform.

MakerDAO’s Spark Protocol to plot cross-chain expansion.

The launch on Gnosis Chain is important as DAI is the native tax token of Gnosis Chain. Hence, the demand for DAI on that chain will scale as Gnosis Chain is growing adoption. Increased transaction volumes will result in elevated demand for DAI.

The expansion to Gnosis Chain comes as Spark Protocol increases the debt ceiling from 200m to 400m DAI.

In an effort to expand across even more chains, zkSync has published a forum post requesting Spark Protocol to also launch on Era Mainnet.

Maple Finance is shutting down undercollateralised lending whilst Goldfinch is struggling with the Tugende loan default.

Maple initially launched with a focus on undercollateralised loans, but due to the prolonged bear market in crypto, the creditworthiness of potential borrowers declined. Only 10% of Maple’s current loans are under-collateralised highlighting the shift to overcollateralised lending. Undercollateralised lending just does not show a viable path to profitability in the current market environment.

Maple was designed to connect vetted institutional lenders and borrowers, gaining popularity with crypto market makers. By May 2022, the total value of Maple's crypto deposits was nearing $1 billion. But challenges arose when Orthogonal Trading defaulted on a $36 million loan in December 2022, leading Maple to cut ties with them. By March, the total crypto value on Maple's platform dropped to $21 million.

In the context of defaults on undercollateralised loans, Goldfinch is battling out a credit event in public and real time: Goldfinch recently faced an issue when Tugende, a motorcycle taxi financing company, defaulted on a $5m loan in February, violating their agreement terms. In response, Goldfinch is considering using $1m from its treasury to compensate lenders for the loss.

This proposal contradicts the protocol's original objective: In undercollateralised lending, lenders assume higher risks, and defaults are expected. By covering Tugende's losses, Goldfinch might establish an unfavorable precedent. If future borrowers default, it raises the question of whether lenders should bear the loss.

RWA.xyz published a lengthy tweet thread highlighting how distressed debt investing mindset could apply to Goldfinch’s credit portfolio as the FIDU token trades at a discount to NAV. The entire analysis can be found here.